TABLE OF CONTENTS:

3. Web3 Gaming is Now Officially Under-Hyped

4. Exploring MEV with Flashbots

8. Portfolio Spotlight :: Omni

A **POSITIVE** BLACK SWAN[1]

Closing out the Bloomberg Invest panel, the moderator asked me what black swans we should expect. I wanted to share my response:

Carol Massar: “We’ve lived in a year, or a couple of years, where I think there are things that just keep happening that we thought never would happen. Pandemic…complete shutdown…financial crisis. Dan, let me ask you, what’s the black swan event that you think, when we talk about stress points, that we should keep on our radar?”

Dan Morehead: “Yeah, I used to sit next to [your previous speaker] Nassim Taleb on a Wall Street trading desk a long time ago.

“Everybody ignores black swans until one happens. Then all everybody wants to talk about is ‘the next shoe to drop’. I would say the biggest surprise is that we already had all these massive shoes drop last year – and it’ll be nothing crazy happening.

“But if you make me say something, I would say regulatory clarity is the one thing nobody’s expecting. There are a few ways that could happen.

“[There’s a three-year lawsuit going on with the SEC and Ripple Labs…. The ruling could drop at any time, and it will definitely drop within the next two or three months.

“We’ve been an investor in Ripple since day one, and I don’t have any inside information, but it’s like 50/50, right? That Ripple wins.]”

Carol Massar: “That could be the black swan?”

Dan Morehead: “That could be the positive black swan that we’re all concerned about. The next ‘shoe to drop’ could be a nice thing.”

Carol Massar: “Nice flip on that. How about Jay?”

Jay Clayton: “No, I’m going to agree with Dan that we have these positive and negative inflection points.”

It happened – a nice black swan.

Here are the key takeaways from the court’s decision:

“XRP, as a digital token, is not in and of itself a security.

“Sales of XRP on exchanges are not securities.

“Sales of XRP by executives are not securities.

“Other XRP distributions – to developers, to charities, to employees are not securities.

“To the extent we made institutional sales direct to institutional buyers (in the US), those did constitute securities.”

– Brad Garlinghouse [excerpt from an email to shareholders, advisors, and friends]

MANY SALES OF XRP WERE NOT SECURITIES :: AN OVERVIEW OF THE RULING

Co-authored by Andrew Harris, Senior Platform Associate, and outside counsel

[For those interested in the details of the ruling on XRP, we’ve partnered with outside counsel to summarize the details. If you’re familiar with the ruling, feel free to skip to the next section or refresh yourself by reading the TL;DR at the bottom.]

On Thursday, July 13th, the District Court for the Southern District of New York ruled that several sales of the XRP token by its issuer, Ripple, were not securities. Crypto market participants will welcome the ruling, which may likely significantly hamper or delay the Securities and Exchange Commission’s ongoing enforcement efforts against crypto issuers and trading platforms. But precisely for that reason, it’s also likely the SEC may appeal ― in other words, the SEC v. Ripple saga may not be over just yet.

The decision comes out of cross-motions for summary judgment by the SEC and Ripple. The Court reviewed four distinct sales or distributions by Ripple of its native XRP token:

– First, XRP sales by Ripple, through wholly owned subsidiaries, to a number of institutional buyers (the “Institutional Sales”);

– Second, XRP sales by Ripple on crypto exchanges “programmatically,” or through the use of trading algorithms (the “Programmatic Sales”);

– Third, XRP distributions by Ripple to various employees, as compensation, or to fund third parties that would develop new applications for XRP and the XRP blockchain ledger (the “Other Distributions”); and

– Fourth, XRP sales by Ripple’s CEO and Chief Legal Officer, in their individual capacities, on crypto exchanges (the “CEO/CLO Sales”).

District Judge Analisa Torres applied the now-famous Howey test to hold that while the Institutional Sales were sales of investment contracts, and therefore sales of unregistered securities; the Programmatic Sales, the Other Distributions and the CEO/CLO Sales did not constitute sales of securities. The Institutional Sales were investment contracts under Howey because institutional investors purchased XRP with the expectation that they would derive profits from Ripple’s efforts. Ripple pooled the money received from institutional investors to promote and increase the value of XRP by developing uses for XRP and protecting the XRP trading market in various ways, Judge Torres found. Ripple’s overall messaging to institutional buyers emphasized the investment potential of XRP and its relationship to Ripple’s efforts. These, and other factors, led Judge Torres to conclude that the Institutional Sales amounted to sales of unregistered investment contracts, in violation of the Securities Act.

Judge Torres reached a very different conclusion on the other three types of sales or distributions. She concluded that while buyers in the Institutional Sales reasonably expected that Ripple would use the capital it received to improve the XRP ecosystem and increase the price of XRP, XRP buyers in the Programmatic Sales did not have the same expectations. The Programmatic Sales were “blind bid/ask transactions,” and buyers in these sales “could not have known if their payments of money went to Ripple, or any other seller of XRP.” Accordingly, “the vast majority of individuals who purchased XRP from crypto exchanges did not invest their money in Ripple at all,” concluded Judge Torres.

It was not enough, observed Judge Torres, to hold that many buyers in Programmatic Sales purchased XRP with an expectation of profit ― what mattered was that they did not buy with the expectation of profit from Ripple’s efforts, because they did not know they were buying XRP from Ripple. Judge Torres also noted that there was no evidence that the buyers in the Programmatic Sales, who were less sophisticated than the institutional buyers, “could parse through” Ripple’s multiple, varying statements marketing XRP to form an expectation of profit. Because the buyers in the Programmatic Sales had no expectation of profit based on Ripple’s efforts, Judge Torres concluded that the XRP sold in the Programmatic Sales were not investment contracts under the Howey test.

The Other Distributions of XRP to employees, third party developers and others were also found to not be investment contracts. Judge Torres noted that the recipients of XRP in the Other Distributions had not paid for the XRP they received, and had in fact been paid XRP by Ripple ― there had therefore been no investment of money as required by the Howey test. Nor was there any evidence that “Ripple funded its projects by transferring XRP to third parties and then having them sell the XRP,” because Ripple never received any payment from these XRP distributions.

Finally, the CEO/CLO Sales were also not investment contracts, for the same reason that the Programmatic Sales were not investment contracts. The CEO and CLO did not know to whom they sold XRP, Judge Torres found, and the buyers did not know the identity of the sellers. Therefore, these purchases were not made with an expectation of profit based on Ripple’s efforts, and so could not be investment contracts.

The TL;DR:

Is XRP a security?

Well…it depends. Judge Torres makes it clear that XRP, as a digital token, is not in and of itself a “contract, transaction[,] or scheme” that embodies the Howey requirements of an investment contract.” Rather, we’d have to look at the how XRP was sold in each transaction. It’s the circumstances under which XRP is sold that determines whether the transaction is an investment contract, and therefore a security. The Court makes no finding as to the security status of XRP itself.

Is XRP sold on a crypto exchange not a security?

Right, or at least the XRP sales on a crypto exchange that the Court reviewed (the Programmatic Sales) were not securities. It seems like the SEC would have to show that (1) buyers on a crypto exchange knew they were buying from the issuer of the asset, and (2) also show that the buyers expected to profit from that issuer’s efforts. This, the SEC failed to do for the XRP in the Programmatic Sales.

Does this mean that most crypto assets sold on an exchange would not be securities?

Don’t pop the champagne just yet, but that’s likely the conclusion that a lot of market participants will reach. Most crypto trading is anonymized, or pseudonymized, and it seems reasonable to think that most buyers and sellers on an exchange don’t know who they are interacting with.

Are U.S. crypto exchanges likely to resume trading XRP?

There’s a pretty good chance that many crypto exchanges will do (exchanges such as Coinbase, Kraken, and Gemini already have), or try to do just that. The XRP price, which had been flatlining for some time, shot up after the Court’s ruling.

What else is next?

This was the SEC’s first ever loss on the security of a crypto asset, and it was likely that they would appeal. On August 18th, the SEC requested permission to appeal the ruling that XRP sales through exchanges didn’t violate securities law, which judge Torres approved.

What does this mean for Coinbase, Binance, and the raft of other crypto exchanges that the SEC has sued, is in the process of suing, or is investigating?

Good news, for now. For one thing, the Binance action is in the SDNY, just like the Ripple case, so that matter is likely to be directly impacted by this ruling. Defendants in other crypto actions by the SEC in other jurisdictions will also likely take note of the ruling, and likely try to pick up on Judge Torres’ findings. At the very least, this ruling slows down the SEC’s efforts, and buys valuable time for the beleaguered U.S. crypto industry.

![]()

WEB3 GAMING IS NOW OFFICIALLY UNDER-HYPED

By Matt Stephenson, Head of Cryptoeconomics

Early approaches to Web3 gaming had mixed success. The single metaverse vision was always dystopian and play-to-earn, which had questionable economic foundations, foundered after a few early successes. And while in-game item economies transacted via the blockchain presented a reasonable approach, it required the game designers to sacrifice control over their in-game economy. Despite these false starts, I believe Web3 still has much to offer the gaming world. I will focus on two areas where I think Web3 would be straightforwardly beneficial to games, right now:

– Digital Property Rights for Memorabilia

– Market Information for “Shapley Valued” Game Design

Memorabilia in e-Sports

In the world of physical sports, we have countless examples of memorabilia taking on value far exceeding their material worth due to their provenance. Consider Michael Jordan’s jerseys: while there are innumerable replicas available for purchase, there’s a singular distinction reserved for the one he wore during the first game of his last NBA Finals series. A good quality replica Michael Jordan jersey can be had for around $100, but this particular piece of history — the jersey worn during that memorable NBA finals series — costs $10.8 million.

Why should the world of e-sports be any different? It’s a domain filled with its own legends, triumphs, and narratives. Just as we did with Michael Jordan’s jersey, we should make the same distinction between, say, the skin an e-sports star wore during the finals of a championship and a ‘visually identical’ skin that wasn’t part of that moment. NFTs create both the “objectness” and the provenance required for such memorabilia.

What’s especially appealing about this approach is its seamless integration into the existing structure of the gaming industry. Utilizing NFTs to assign unique value to e-sports memorabilia doesn’t necessitate a relinquishment of control over the in-game economy by the game designers. It’s an addition that enriches the existing landscape rather than uprooting it.

The Informational Benefit of Markets

One of the appeals of e-sports memorabilia is that it allows game designers to do “business as usual.” And business as usual is, let’s face it, creating command economies where they try to control the flow and value of all the items.

Command economies have their benefits (at least to the people in charge!) but markets have some advantages too. One advantage is that market prices are incredible channels of reliable information, and this information can used to improve the product itself. It turns out that the InfiniGods does exactly this, using market prices to inform and iterate over their approach.

If you could see into the mind of a great game designer, like those at Infinigods, you’d likely see something that looks like a Shapley Value. The equation is a gigantic, Nobel-prize-winning, thing that looks like this:

But what it says in game design is simple: the value of a game item is how much value it adds in all relevant situations.

Imagine you’re playing a shooter where enemies have 110HP, and your weapon is a bow that does 100HP worth of damage. If you have an upgrade that increases your bow’s damage by 10%, how much is that upgrade worth? The bad game designer says “10%”, the good game designer, consciously or not, uses a Shapley Value.

The Shapley Value gives the boost credit for taking you from “two shot kill” to “one shot kill”. That “small improvement” actually makes your bow twice as good!

Shapley gives us the value of the bow. And if there are markets in your goods then you can use the Shapley Value to compare. Is an item is trading at a discount to its use value? At a surplus? This allows for rich, explanatory, data analysis that can be used to improve the game experience.

Web3 Features Will Win Out

The potential benefits of Web3 in the gaming industry transcend mere hype or surface-level interactions. Two concrete applications – utilizing NFTs to assign unique value to e-sports memorabilia and harnessing market information to inform game design – illustrate this. By recognizing the inherent value of digital objects and utilizing the informational wealth of markets, we can deepen player engagement, enhance game economies, and add layers of richness to gameplay. As we continue to explore the possibilities of Web3 gaming, we’re not merely envisioning a more immersive gaming landscape; we’re actively constructing it.

![]()

EXPLORING MEV WITH FLASHBOTS

Our Head of Cryptoeconomics, Matt Stephenson, discussed everything Maximal Extractable Value (MEV) with Quintus Kilbourn of Flashbots, including an overview of their new architecture, SUAVE. We wanted to share the full-length recording of the discussion, but also some of the highlights below.

Context:

MEV is a controversial strategy used by miners/validators to extract value on-chain by including, excluding, or changing the order of transactions during the block production process. It is estimated that over $700mm has been extracted on Ethereum alone.

Flashbots is a research and development organization formed to mitigate the negative externalities posed by MEV.

Matt: “Have you ever tried to explain MEV to your grandmother and, if so, how did you do it?”

Quintus: “I don’t know if it was that successful, but they told me they were proud of me. So I’m relatively happy with it. The high-level explanation for someone who knows what blockchains are, is that – I guess you could maybe even start outside of blockchain – often when we find ourselves in some sort of coordination setting, we have some central coordinator who we give power and we say, ‘Hey, let’s organize what’s going on’. So we have the central bank or banks that control traditional finance or money supply and these kinds of things. This is how we generally coordinate. But the problem with this is that this central monopolistic party has a lot of power and they could be corrupted or abuse power for their own game.

“And although blockchain really has tried to address this, [for example] Bitcoin came out and said, ‘okay, we don’t want control over monetary policy or to be in the hands of a single party or maybe I don’t want someone to be able to take money out of my bank account’. And of course, Ethereum went way past that. What MEV is looking at now is this much narrower scope in which there are central parties [miners/validators] which have a lot of influence and are able to extract value from their powerful position.

“And more specifically how this tends to happen on blockchains like Ethereum is you have for 12 seconds, or however long the block time is, you have one party who ends up controlling how transactions interact with the blockchain. And so, for example, they can reorder transactions if they see someone’s buying something, they might buy ahead of them, front run them, or they might capitalize an arbitrage. Some definitions of MEV also take into account reorgs and these kinds of things, which can be very profitable. But I think if you had to encapsulate it in one sentence, it [MEV] is used as a reference to the total amount of value which can be extracted by a block producer who’s turn it is to produce a block.

“The key point there being: can be extracted. It’s sort of a theoretic concept. It’s not all the value that is extracted, but in theory when it’s possible”.

Matt: “So we can think of MEV as value that accrues due to someone’s privileged access to a scarce resource which is blockspace. But Google is an interesting point of comparison here – they too have a scarce resource that generates value for them, the ad space at the top of their search results. Talk about the recent lawsuit against Google and how it compares with “MEV.”

Quintus: “Yeah, it’s actually a really good analogy. The case came out in I think January this year, or at least the recent version of it. And basically, it’s addressing the two-sided markets – the ad markets that Google runs. So, it’s not just Google search results, but more generally websites that have real estate for ads on one side of the market and then advertisers on the other. It’s a relatively complex case and at the moment it’s just all accusations. You can’t really say anything with certainty. But the very high-level point of view is that Google is accused of using it’s privileged access to data in the opaque auction system which they run to benefit themselves and do this at the cost of the participants in their system. But also, they were manipulating this auction supposedly to push out competition to make sure that they maintain a monopolistic position in the market.

“And of course, the incentive to do this, in the eyes of the antitrust cases, is to extract rents and make a bunch of money. And the reason they’re able to do this at the moment is they exist in the full stack. They run software for the bidders, they run software for the websites where the ads are going to be shown, they run the exchange in the middle or an exchange in the middle and make sure there’s a lot of synthesis between these things. And there’s a variety of accusations, but generally [they are] leveraging that monopolistic position to extract value – that’s the accusation.”

Matt: “So one of the cool things about Flashbots to me, is that your story makes you feel a little bit like you’re brave firefighters who came out to battle this centralizing MEV blaze. And that’s true. But you’ve also emerged with this general purpose solution to make fewer things catch on fire, and make them easier for you to put out when they do. So tell us about SUAVE.”

Quintus: “Yeah, so I think your characterization is pretty good. We started thinking more specifically about this, so of the impacts of MEV on validator revenues and then on specific use cases and SUAVE is the generalization of this. SUAVE says, ‘okay, well we have this more general problem that’s leading to all of these different issues. How do we address this? How do we deal with this?’ SUAVE isn’t a specific solution to this, but rather like a platform. So we say, ‘okay, well really what people need is some sort of platform where people can deploy solutions for different use cases.’

“And so more specifically, what ends up happening is we see users now realizing that they don’t have sufficient information on their own to be able to execute effectively in the current blockchain paradigm. They have set the slippage limit, they don’t know what the prices they should be expecting is depending on the application, there are different things that come to mind. Maybe it’s better for them to execute in a batch, maybe it’s better for them to outsource execution to a sophisticated party.

“What ends up happening is that a lot of off-share infrastructure ends up forming. So you have CoW Swap is an example, it’s a batch auction. They run a server, you submit a limit order to them, they aggregate these limit orders, they run an auction basically for market makers to clear this batch basically either with their liquidity on chain or with active liquidity. Well, which would still be on chain but not in a DEX. That’s one example. Uniswap just came out with UNIX, which is something similar, which is sort of an RFQ kind of system. There’s a couple of different use cases. I’m sticking with the swap examples. Those are the most prevalent and the easiest to understand.

“And what SUAVE does is we say, ‘okay, well really what we’re doing is we are reintroducing the problem we had from the beginning. We’re introducing these monopolists who now have an ability to extract some rent, do things that serve them potentially at the cost of users. And it’s now this trust-based game where people have to monitor if these guys are all breaking the rules. And this is in fact two problems. One is the MEV direct problem where these parties can extract value. And the other problem is that it requires a lot of trust for users to actually interact with these parties. And what this means is that if I want to compete and I say, ‘oh, this batch auction is not as good as it could be, I want my batch auction prime, I think it’s better’. It’s very hard for me to get that set up because now I have to go around and convince users of wallets and things that, ‘Hey, I’m not going to steal your money, please send it to me’.

“And that’s not too different from what we’ve seen in the traditional world where it takes months or a lot of time to get your licenses and these kinds of things. And it really, I think stifles innovation because there’s very high barriers to entry and that’s in the end not good for users. And so what we’d like to do is, or what we are currently working on doing, is providing the SUAVE platform which allows this off chain infrastructure that isn’t bottle necked by consensus to run in a more trustworthy way. And what do I mean by trustworthy in a better way?

“We want it to be both decentralized so different artists can run it and it’s geographically decentralized even though the logic is still the same. And also for it to be more trustworthy because you know that the code which is being advertised, this batch auction, whatever, is actually what’s being executed. And I can get into details later, but that’s the high-level thing. And so instead of having this batch auction run on someone’s server, having Uniswap X run on someone’s server, ideally these things are deployed on SUAVE and so it’s executed in a distributed way, but users know that because we have this smart contract interface that what these guys are advertising is actually what’s happening.”

Matt: “I don’t know if you know there’s been this Taylor Swift debacle with ticket pricing and trying to auction that stuff off. Could you say in SUAVE, again, you don’t have to say you do it for Taylor Swift, but if you would tell us, ‘I want the closest floor tickets to the stage with no obstructive view and I’m willing to pay $300’ or something like that. Is that kind of an intent based way to think?”

Quintus: “Yeah, I think the sort of phrase ‘expressing intent’ has taken on a lot of different meanings in the crypto Twitter discourse. But yeah, I think that’s certainly something that you could express with SUAVE. I think it’s very similar to the Google case where you want to run around some kind of auction, you have codified rules, you have ways in which people want to interact with it, the information might be sensitive, the sort of competition for the opportunity to have access to whatever the scarce resource is. And so I think SUAVE would actually be a very ideal home for this. That being said, you have currently scalability questions and so hopefully in a couple of years time we can be talking about the concert we attended and how we got our tickets on SUAVE and how cool that is. But I think in the near future I’ll focus definitely a bit more blockchain application focused.”

Matt: “I think that’s prudent, but it is good now but, right? I mean it is a more general problem than just the blockchain thing and I think there’s obviously been this kind of race to have the most galaxy brain take on he is, and I think we’ve done a good job more or less avoiding that. But I think part of where it comes from is a legitimate place, which is the fact that yes, we are solving these very specific sorts of things. What you’re doing is solving a very specific problem, but the general applicability is there. It almost in a lot of ways, going back to your first point about what Bitcoin was trying to do, it feels almost a little bit like the last mile problem for blockchains where we got a lot of decentralization up to the point of a block and now how do we solve this type of last mile problem of, well, what is the centralization vector and what is the sort of value extraction that happens within that little concentrated area of power?

“And the field like SUAVE is addressing that in a really exciting and cool way that SUAVE chains, but obviously can go much beyond once we solve scalability, but it’s happening, we’re fine, we’re good on that.”

![]()

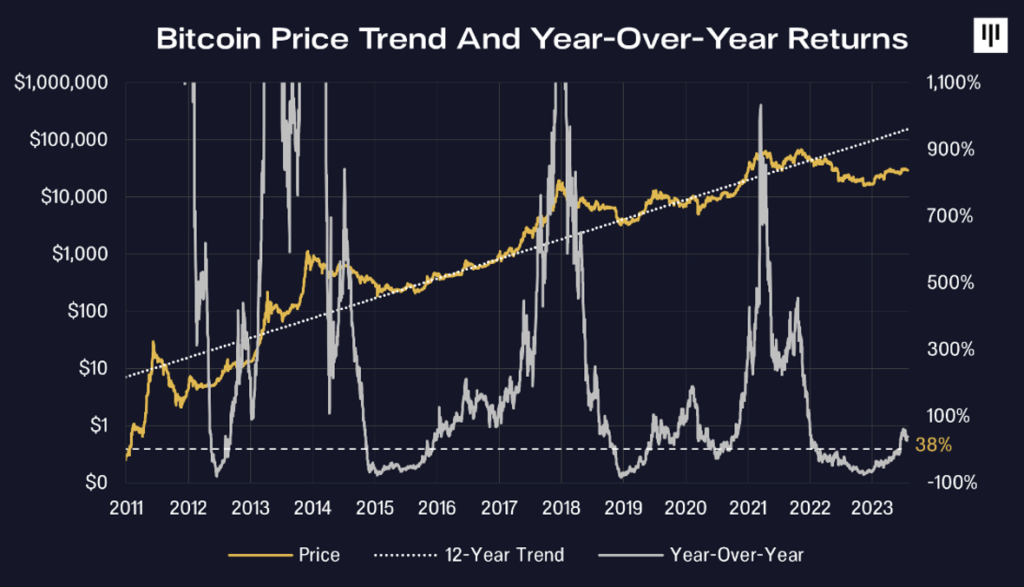

LONGEST PERIOD OF NEGATIVE YEAR-OVER-YEAR RETURNS

Bitcoin experienced the longest period of negative year-over-year returns in its history, lasting 15 months (2/8/22–6/12/23).

The longest period prior was just under a year (11/14/14–10/31/15).

Our view is that we’ve seen enough – there’s just so long markets can be down.

We believe the combination of recent positive events – the XRP ruling and endorsements by BlackRock et al. – in addition to the Bitcoin Halving expected to occur in April 2024, provide a strong setup for the next bull market for digital assets.

BITCOIN HALVING :: CONTEXT

The money supply function of the Bitcoin protocol is the polar opposite of Quantitative Easing. The Bitcoin code states a total of 21 million coins will be released and the supply of new coins will decrease over time.

Today 6.25 bitcoins are issued every ten minutes. There’s no “Greenspan put” if a politically-powerful group like homeowners or people who own equities is suffering. It’s just 6.25 BTC every ten minutes.

Every four years that “block reward” is cut in half, thus it’s referred to as “the halving”. This process repeats until the year 2140 A.D., when the Zeno’s Paradox ceases at 21 million bitcoins.

Bitcoin’s supply and coin distribution ruleset is based purely on mathematics – predictable and transparent by design.

“Total circulation will be 21,000,000 coins. It’ll be distributed to network nodes when they make blocks, with the amount cut in half every four years. First four years: 10,500,000 coins. Next four years: 5,250,000 coins. Next four years: 2,625,000 coins. Next four years: 1,312,500 coins. Etc. . . .”

— Satoshi Nakamoto, The Cryptography Mailing List, January 8, 2009

NEXT YEAR’S HALVING

The next halving is projected to occur on April 20, 2024. The mining reward will decrease from 6.25 BTC per block to 3.125 BTC per block.

Efficient Markets Theory would hold that if we **all** know it’s going to happen, then it has to be priced in. Paraphrasing a line attributed to Warren Buffet on the dogma, “The markets are almost always efficient, but the difference between almost and always is $80 billion to me.” Thus, even if we think everybody knows something, it doesn’t mean there isn’t a ton of money to be made.

“Investing in a market where people believe in efficiency is like playing bridge with someone who has been told it doesn’t do any good to look at the cards”

— Warren Buffet, 1984, as cited by Davis, 1990

If the demand for new bitcoins stays constant and the supply of new bitcoins is cut in half, this will force the price up. Previously, there has also been an increased demand for bitcoin before the halving event because of the anticipation of a price increase.

Over the years we have stressed that the halving is a big event – but it takes years to play out.

Bitcoin has historically bottomed 477 days prior to the halving, climbed leading into it, and then exploded to the upside afterwards. The post-halving rallies have averaged 480 days – from the halving to the peak of that next bull cycle.

IF history were to repeat itself, the price of bitcoin should have troughed December 30, 2022.

The actual low occurred on November 9th, 2022 amidst the FTX fiasco – a month and a bit early.

We would then see a rally into early 2024 and then a strong rally after the actual halving. The following chart shows what might happen if Bitcoin repeats the performance around previous halvings.

The current price of bitcoin is outpacing our projection to $28,200/BTC at the halving date, now 21% above that forecast.

BITCOIN HALVING :: STOCK-TO-FLOW PRICE PROJECTION

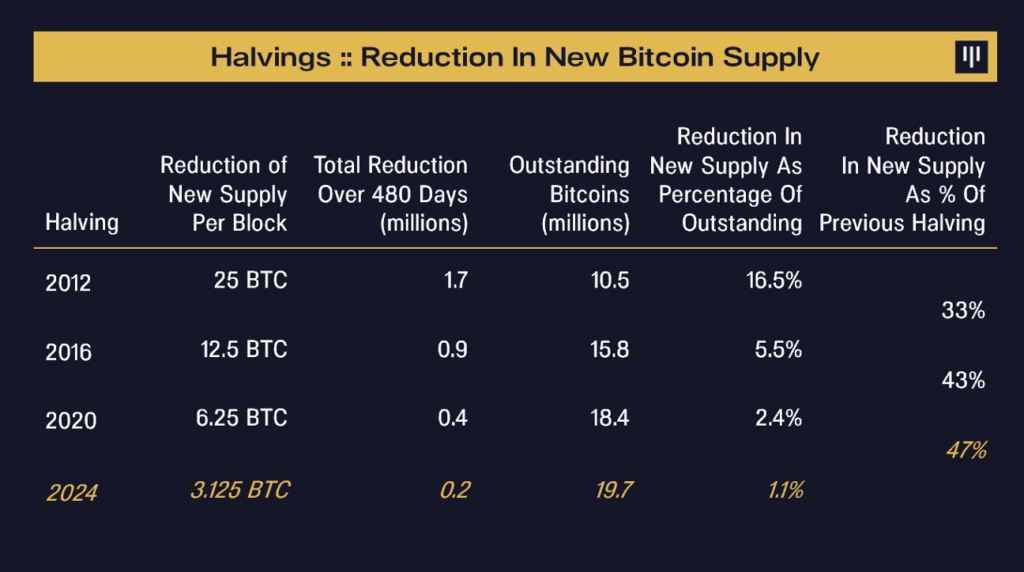

The framework we’ve used for analyzing the impact of halvings is to study the change in the stock-to-flow ratio across each halving. The first halving reduced the supply of new bitcoins by 17% of the total outstanding bitcoins. That’s a huge impact on new supply and it had a huge impact on price.

Each subsequent halving’s impact on price will likely taper off in importance as the ratio of reduction in the supply of new bitcoins from previous halvings to the next decreases. Below is a chart depicting past halvings’ supply reductions as a percentage of the outstanding bitcoin at the time of the halving.

The 2016 halving decreased the supply of new bitcoins only one-third as much as the first. Interestingly, it had exactly one-third the price impact.

The 2020 halving reduced the supply of new bitcoins by 43% relative to the previous halving. It had a 23% as big an impact on price.

The next halving is expected to occur on April 20, 2024. Since most bitcoins are now in circulation, each halving will be almost exactly half as big a reduction in new supply. If history were to repeat itself, the next halving would see bitcoin rising to $28k before the halving and $117k after.

![]()

10TH ANNIVERSARY BLOCKCHAIN SUMMIT :: HIGHLIGHT VIDEOS

Over the past few blockchain letters, we’ve released full-session recordings from our 10th Anniversary Summit.

This month, we’d like to share highlight videos covering some of the most widely-discussed topics in the cryptocurrency ecosystem today.

Check them out below!

![]()

PORTFOLIO SPOTLIGHT :: OMNI

Co-authored by Omni, Paul Veradittakit, and Andrew Harris

The Problem

Ethereum has long been the gold standard for dApps, smart contracts, and the wider crypto ecosystem. Yet, its scalability issues have posed significant challenges, leading to the emergence of rollups as a solution to enhance transaction speed and efficiency. While L2 scaling solutions promise to absorb all of Ethereum’s activity at lower cost, they’re not without their drawbacks. The adoption of L2s has directly led to a fragmented Ethereum landscape, breaking the once unified ecosystem into an array of smaller, isolated platforms.

For developers, this fragmentation means that when they create an app on a specific rollup, they can only serve a small subset of the broader crypto audience. If developers attempt to bridge their apps across multiple rollups to reach a broader audience, they increase complexity of the user experience, increase development overhead and fragment their liquidity.

We have solved high transaction fees, but it has come at the cost of fragmentation. How do we empower developers to build affordable applications without substantially limiting their addressable user base?

Enter the Omni Network

Omni is a development platform that connects Ethereum’s entire L2 ecosystem. Developers can now build applications that function across multiple L2s, reaching every user and accessing all resources without worrying about fragmenting liquidity. In essence, it offers the best of both worlds: access to a wider user base in a way that enhances liquidity network effects instead of breaking them.

Omni not only solves this problem for developers — it also fundamentally changes the experience for end users. Gone are the days of endless complex bridging tasks. With Omni, users can effortlessly tap into the latest DApps, regardless of which rollup they are connected to or where they hold their capital. Omni removes the friction of forcing users to interact with bridging and all the complexities involved in cross-rollup activity — apps appear as if they are natively present on other rollups at an interface level while behind the scenes, all data and value is transferred to the core application without forcing the user to think about any of that. Omni expands the addressable market to all of Ethereum’s users without adding any friction to the UX. It’s all about simplicity and accessibility.

Innovations in Security

Omni was designed with the following question in mind:

“What would it look like if the core Ethereum protocol facilitated communication across all L2s?”

Taking this approach, the Omni Network derives security directly from Ethereum L1 itself. Through focusing on the Ethereum ecosystem, it can always leverage Ethereum L1 as the core arbiter of truth because all rollups post their data to Ethereum. This design introduces a radically superior standard in security.

This component of the protocol is only made possible through a close partnership with EigenLayer. Through leveraging restaking, Ethereum validators themselves are the ones responsible for sourcing data from all L2s and aggregating that information together to create a secure infrastructure layer that empowers developers to access all of Ethereum’s users.

Omni’s Growth

The Omni Network has managed to become one of the fastest growing projects in this bear market. Through the team’s relentless focus on building deep within the protocol stack to abstract away complexity at every level they are bringing to market a product that promises to serve as one of the most important infrastructure layers for the future of Ethereum. The first testnet already has over 1 million transactions, 100k active users and their community has grown to over 200k on twitter.

With our long focus on pioneering infrastructure projects, we are proud to have led both of Omni’s fundraising rounds bringing their total raised to $18M alongside other leading investors like Two Sigma Ventures and Jump.

You can learn more about Omni via their website or follow them on Twitter.

![]()

2023 COMPENSATION SURVEY

We’re running a compensation survey to bring more transparency to the crypto ecosystem. If you work in Web3 or even Web2, and want to participate, it takes five minutes to be a part of our 2023 compensation survey here.

We’ll be sharing the anonymized data set with participants at the end.

Thanks to everyone who has submitted thus far!

![]()

Good luck out there,

“Put the alternative back in Alts”

PANTERA CONFERENCE CALLS[2]

Our investment team hosts monthly conference calls to help educate the community on blockchain. The team discusses important developments that are happening within the industry and will often invite founders and CEOs of leading blockchain companies to participate in panel discussions. Below is a list of upcoming calls for which you can register via this link.

Pantera Liquid Token Fund Investor Call

Tuesday, August 22, 2023 11:00am PDT / 20:00 CEST / 2:00am Singapore Standard Time

Open only to Limited Partners of the fund.

Investing in Blockchain Conference Call

A discussion of the blockchain opportunity set and how Pantera’s funds are structured to capture value in the current and evolving market environment.

Tuesday, September 12, 2023 9:00am PDT / 18:00 CEST / 12:00am Singapore Standard Time

Please register in advance via this link:

https://panteracapital.com/future-conference-calls/

Venture Fund III Investor Call

Tuesday, September 26, 2023 9:00am PDT / 18:00 CEST / 12:00am Singapore Standard Time

Open only to Limited Partners of the fund.

Pantera Blockchain Fund Investor Call

Tuesday, October 3, 2023 9:00am PDT / 18:00 CEST / 12:00am Singapore Standard Time

Open only to Limited Partners of the fund.

Venture Fund II Investor Call

Tuesday, October 10, 2023 9:00am PDT / 18:00 CEST / 12:00am Singapore Standard Time

Open only to Limited Partners of the fund.

Join us in learning more about the industry, the opportunities we see on the horizon, and our funds.

PORTFOLIO COMPANY OPEN POSITIONS[3]

Interested in joining one of our portfolio companies? The Pantera Jobs Board features 1,500+ openings across a global portfolio of high-growth, ambitious teams in the blockchain industry. Our companies are looking for candidates who are passionate about the impact of blockchain technology and digital assets. Our most in-demand functions range across engineering, business development, product, and marketing/design.

Our portfolio companies are actively hiring for the following roles:

-

Omni Network – Senior Blockchain Engineer (Remote)

-

Cega – Software Engineer, Solidity (Remote)

-

Offchain Labs – Product Manager (Remote)

-

Ondo Finance – Sales Director (Remote)

-

Alchemy – Engineering Manager (New York or San Francisco)

-

StarkWare – Senior Software Engineer (Netanya, Israel)

-

Rarify – Head of Developer Relations (Remote)

-

Livepeer – Growth Marketer (Remote)

-

0x Labs – Site Reliability Engineer (Remote)

-

Obol – Validator Relations (Remote)

-

Flashbots – Engineering Manager (Remote)

-

Waterfall – Software Engineer (New York)

-

Injective Protocol – Ecosystem Growth Associate (Remote)

-

CoinDCX – Engineering Manager (Remote)

-

Brine – Infrastructure Engineer (Bengaluru, Karnataka, India)

Visit the Jobs Board here and apply directly or submit your profile to our Talent Network here to be included in our candidate database.

[1]Important Disclosures – Certain Sections of this Letter Discuss Pantera’s Advisory Services and Others Discuss Market Commentary. Certain sections of this letter discuss the investment advisory business of Pantera Capital Management and its affiliates (“Pantera”), while other sections of the letter consist solely of general market commentary and do not relate to Pantera’s investment advisory business. Pantera has inserted footnotes throughout the letter to identify these differences. This section provides educational content and general market commentary. Except for specifically marked sections of this this letter, no statements included herein relate to Pantera’s investment advisory services, nor does any content herein reflect or contain any offer of new or additional investment advisory services. Opinions and other statements contained herein do not constitute any form of investment, legal, tax, financial or other advice or recommendation.

[2]Important Disclosures – This Section Discusses Pantera’s Advisory Services. Information contained in this section relates to Pantera’s investment advisory business. Nothing contained herein should be construed as a recommendation to invest in any security or to undertake an investment advisory relationship, or as any form of investment, legal, tax, or financial advice or recommendation. Prospective investors should consult their own advisors prior to making an investment decision. Pantera has no duty to update these materials or notify recipients of any changes.

[3] This section does not relate to Pantera’s investment advisory services. The inclusion of an open position here does not constitute an endorsement of any of these companies or their hiring policies, nor does this reflect an assessment of whether a position is suitable for any given candidate.

This letter is an informational document that primarily provides educational content and general market commentary. Except for certain sections specifically marked in this letter, no statements included herein relate specifically to investment advisory services provided by Pantera Capital Management Puerto Rico LP or its affiliates (“Pantera”), nor does any content herein reflect or contain any offer of new or additional investment advisory services. Nothing contained herein constitutes an investment recommendation, investment advice, an offer to sell, or a solicitation to purchase any securities in Funds managed by Pantera (the “Funds”) or any entity organized, controlled, or managed by Pantera and therefore may not be relied upon in connection with any offer or sale of securities. Any offer or solicitation may only be made pursuant to a confidential private offering memorandum (or similar document) which will only be provided to qualified offerees and should be carefully reviewed by any such offerees prior to investing.

This letter aims to summarize certain developments, articles, and/or media mentions with respect to Bitcoin and other cryptocurrencies that Pantera believes may be of interest. The views expressed in this letter are the subjective views of Pantera personnel, based on information that is believed to be reliable and has been obtained from sources believed to be reliable, but no representation or warranty is made, expressed or implied, with respect to the fairness, correctness, accuracy, reasonableness, or completeness of the information and opinions. The information contained in this letter is current as of the date indicated at the front of the letter. Pantera does not undertake to update the information contained herein.

This document is not intended to provide, and should not be relied on for accounting, legal, or tax advice, or investment recommendations. Pantera and its principals have made investments in some of the instruments discussed in this communication and may in the future make additional investments, including taking both long and short positions, in connection with such instruments without further notice.

Certain information contained in this letter constitutes “forward-looking statements”, which can be identified by the use of forward-looking terminology such as “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue”, “believe”, or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual policies, procedures, and processes of Pantera and the performance of the Fund may differ materially from those reflected or contemplated in such forward-looking statements, and no undue reliance should be placed on these forward-looking statements, nor should the inclusion of these statements be regarded as Pantera’s representation that the Fund will achieve any strategy, objectives, or other plans. Past performance is not necessarily indicative of or a guarantee of future results.

It is strongly suggested that any prospective investor obtain independent advice in relation to any investment, financial, legal, tax, accounting, or regulatory issues discussed herein. Analyses and opinions contained herein may be based on assumptions that if altered can change the analyses or opinions expressed. Nothing contained herein shall constitute any representation or warranty as to future performance of any financial instrument, credit, currency rate, or other market or economic measure.

This document is confidential, is intended only for the person to whom it has been provided, and under no circumstance may a copy be shown, copied, transmitted, or otherwise given to any person other than the authorized recipient.