HOUSING ALL OF FINANCE: THE RISE OF PERPS AND HYPERLIQUID

Cosmo Jiang, Managing Partner & Cody Poh, Investment Analyst

Perpetual futures, or “perps”, are on a path to becoming one of the dominant trading instruments in global financial markets. Perps are evolving from a crypto-native phenomenon to become a fundamental shift in market structure, and one that traditional investors can no longer ignore. The idea is not new. Its enabling infrastructure has now caught up, in particular onchain in decentralized finance, and as of last week, with a set of actions from the CFTC, the U.S. regulatory system has begun to formally accommodate it.

Perpetual Futures’ Advantages

The first formal futures market was the Dojima Rice Exchange, established in 1730 to facilitate Japanese rice farmers hedging crop price risk. Outside speculators realized they could trade those contracts to take directional bets on the price of rice, on margin with leverage and without taking physical delivery of rice (cash-settled). Capitalism played out as it does, and in due course today futures span all major asset classes (commodities, FX, equities), and the majority of futures trading relates to leveraged, directional bets.

A perpetual future is a futures contract that never expires. In place of an expiry, perps use a funding rate, a small periodic payment (e.g. 1-hour, or most frequently on crypto exchanges 8-hours) between longs and shorts: when the perp trades rich relative to spot, longs pay shorts, and when it trades cheap, shorts pay longs. Basis arbitrageurs step in to tether the contract price to spot. The lack of expiry is a simple-sounding design choice with meaningful benefits relative to existing derivatives (e.g. dated futures and options), including being easier to manage from a practical execution perspective, easier to understand from a risk perspective, and natively 24/7.

From a practical execution perspective, perpetual futures require less management than traditional futures. Traditional futures have expiry dates (e.g. monthly), which is why they’re also often called “dated-futures”. To hold a position over a longer period of time a trader must continuously roll from one contract to the next, sometimes managing a strip of multiple contract expiries each with their own basis between the future and spot. A perp collapses that complexity into one continuous position with no expiries and thus nothing to roll. A trader can hold for seconds or, in theory, forever without needing to worry about managing the trade.

From a risk management perspective, perps are also easier to understand than other derivatives. Dated futures require taking a view on a specific timeframe. With options, which also have a specific expiry, a trader can be right on direction but still lose to time decay or a shift in implied volatility. A perp strips away those complexities and allows a trader to express conviction more directly and nearly solely (although not entirely) on price.

Perps are also always on, trading 24/7 with no market hours and no weekend gaps. For an internet-native user base that lives in an always-on economy with global information connectivity, continuous access is not a feature. It is the expectation. Traditional exchanges are already moving in this direction at the behest of these market demands. Perps are the natural instrument to use if one fast forwards in its current direction.

Given its origins the dated-future is feeling, well, a bit dated. For the directional leveraged exposure most participants want, the perpetual future is a more natural instrument with all the benefits stated above.

Digital Assets Laid the Groundwork for Perpetual Futures

The design of the perpetual future is nothing new, dating back to a 1993 paper by Nobel laureate Robert Shiller. However, existing market structure in traditional exchanges created too much friction to allow it to catch on. Without the baggage of the legacy system and instead by being internet-native, the digital assets industry created the environment for perps to blossom. The detailed mechanics that made perps work were first solved at scale in 2016 to trade Bitcoin by BitMEX, which grew tremendously on the back of this innovation.

Perps have gone on to experience tremendous traction. In 2025, total perps trading volume on centralized exchanges was $62 trillion[1]. This is many multiples of spot volume of roughly $19 trillion and is the majority of the $86tn total derivatives trading volume[2], showing the market’s preference of perps over options.

For most of their history, perps were traded on centralized exchanges (CEX). The more interesting story recently has been the migration on-chain to decentralized exchanges (DEX). There have been many earlier attempts that found some level of success, with the most notable being GMX and Synthetix which used pool-based trading models and DYDX which used a central-limit order book and dedicated blockchain, but each struggled to match centralized venues on latency, liquidity and user experience.

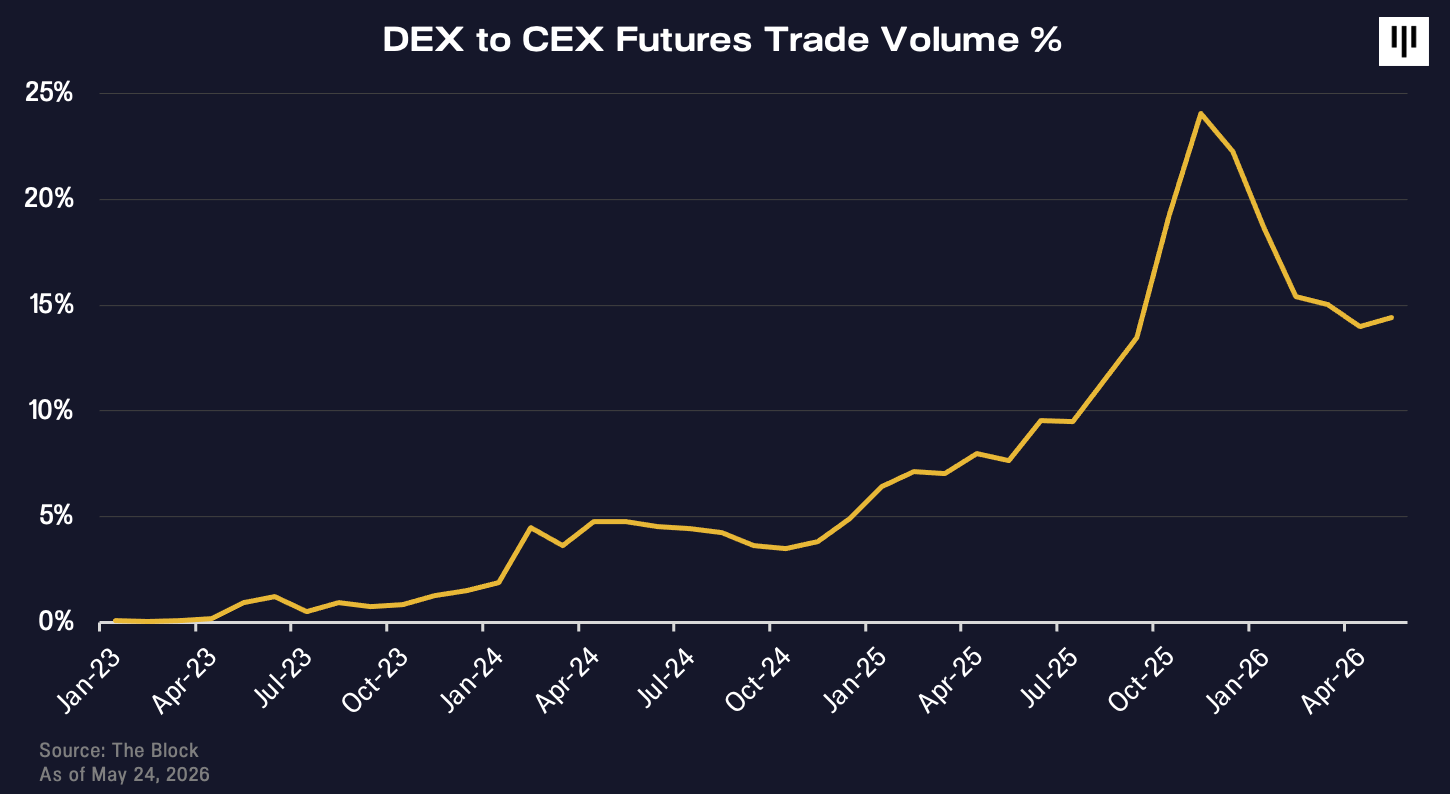

Hyperliquid has taken DEX perps to the next level, meaningfully increasing the market share of onchain perps. DEX perps volumes have reached 14% of CEX perps volumes, up from less than 1% in at the beginning of 2023 when Hyperliquid first launched.[3]

The Rise of Hyperliquid

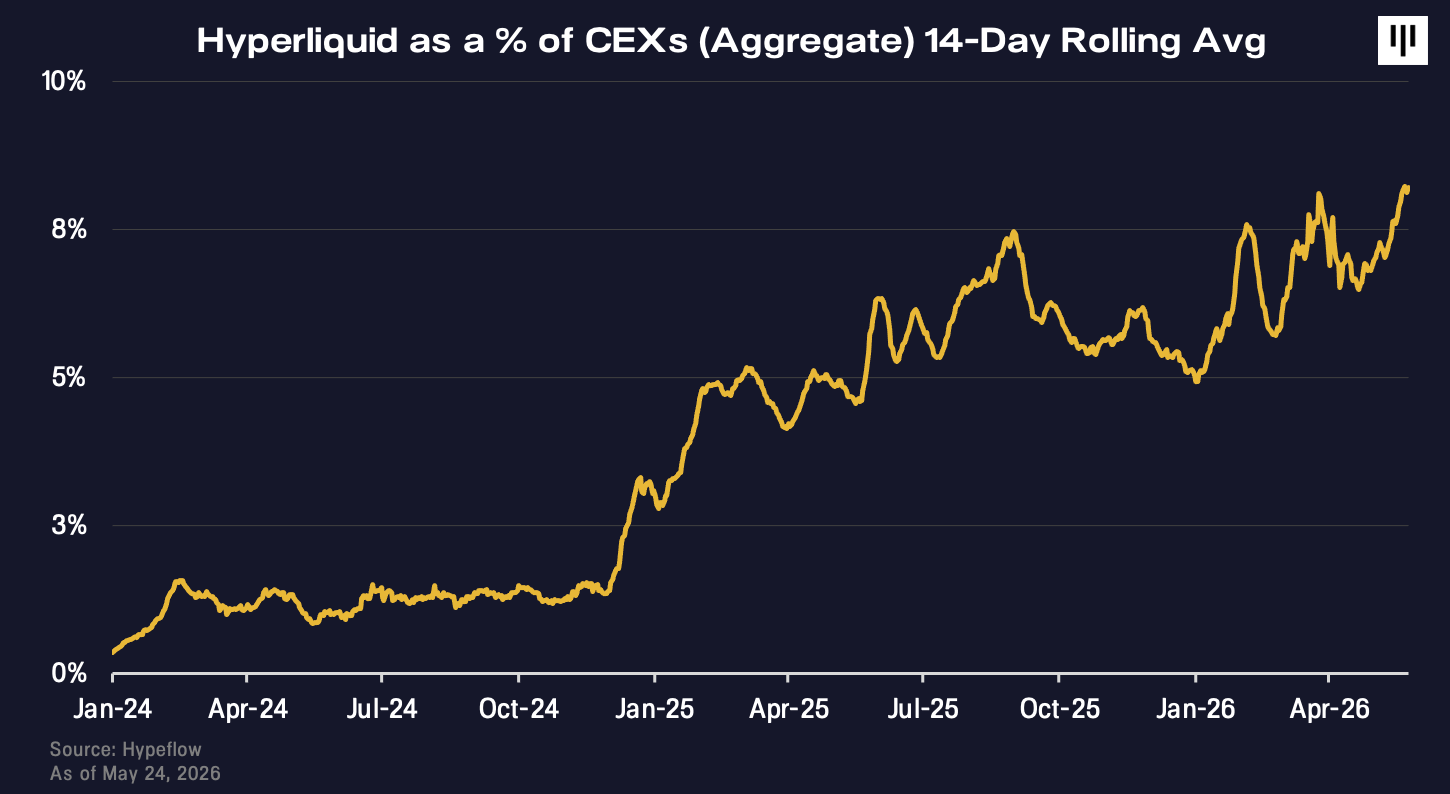

Hyperliquid is the largest decentralized perpetuals exchange, with roughly 40% of on-chain perp volume[4]. Hyperliquid was conceived of by Jeff Yan, a Harvard Math 55 alum and former high-frequency trader who had spent the prior years running an under-the-radar market-making firm, Chameleon Trading. The collapse of FTX was the catalyst for building Hyperliquid; Yan redirected his trading team’s efforts to instead create a decentralized alternative to the centralized exchanges that had just failed their users, acknowledging that existing blockchains were too slow for professional on-chain trading[5].

The team built its own Layer 1 blockchain purpose-built for trading and released it to the world at the end in February 2023. One of these changes included adding a speed-bump like feature that prevented the most aggressive high-frequency trading firms from taking advantage of market makers, hurting near-term transaction volume in favor of healthier growth. To address the cold-start problem that all exchanges face, the team bootstrapped liquidity by opening up their own proprietary trading algorithm for anyone to participate in via an onchain vault called HLP, the Hyperliquidity provider. Giving away this high-performance strategy to the public for free had the added benefit of winning the favor of the community, who became aligned advocates to further bolstering Hyperliquid’s growth. Worried about U.S. regulatory uncertainty regarding decentralized finance and perps, they also relocated to Singapore in Spring 2024, one of many major losses the US suffered as a result of its prior regulatory stance that is now being rectified.

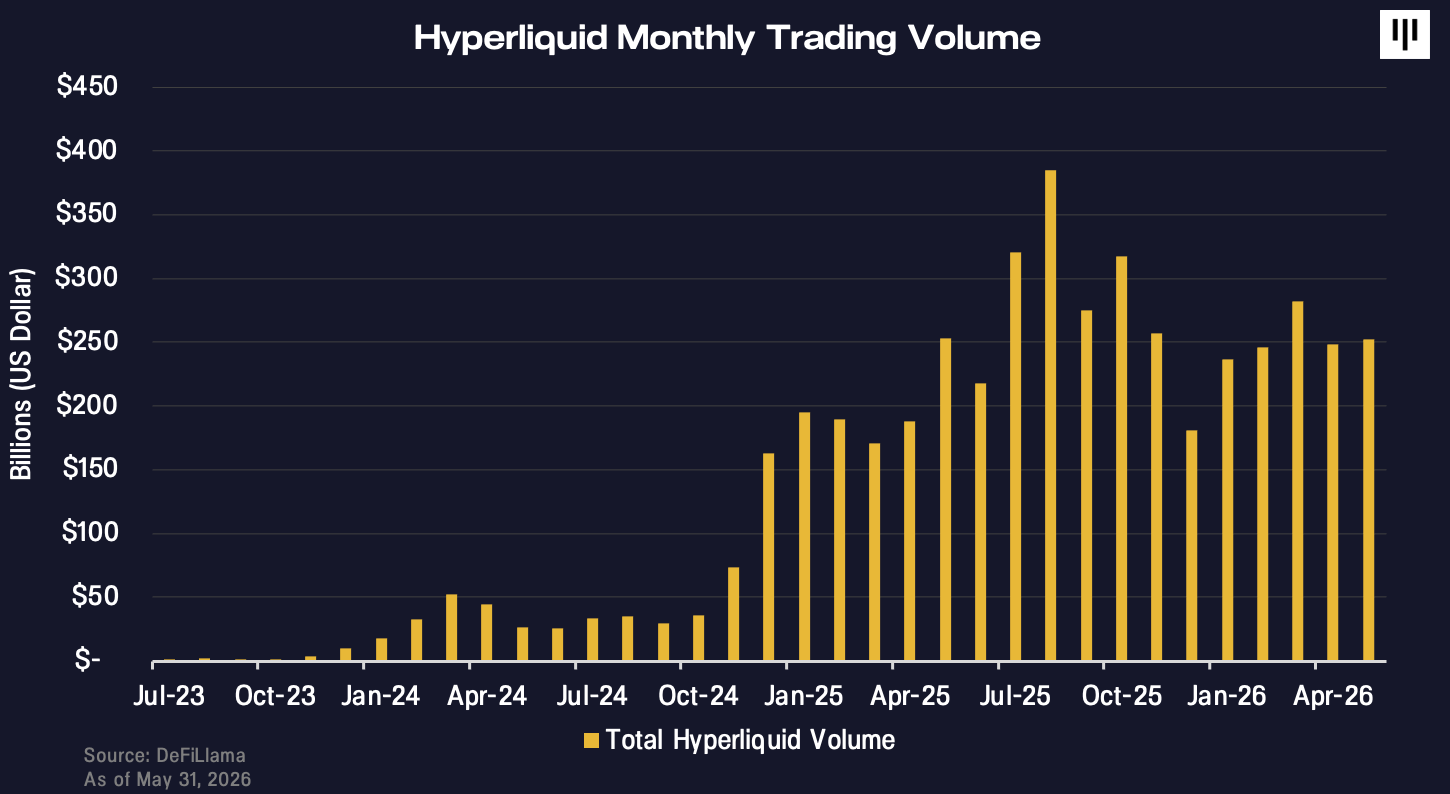

Through a combination of a high talent density core team, a stakeholder alignment ethos that represents the best of crypto’s ideals, and incredible execution Hyperliquid has outran its competition to now be the largest and most profitable decentralized perps exchange with over $250B monthly volume and $800M annualized revenue. Hyperliquid continues to grow trading volumes, over time taking an increasing relative share of volume vs centralized exchanges.

From Digital Assets to “Housing All of Finance”

Hyperliquid’s growth this year has accelerated as it expanded beyond crypto-native assets into equities, commodities, indices and private companies. Jeff Yan has described the vision “Housing All of Finance” on a single venue.

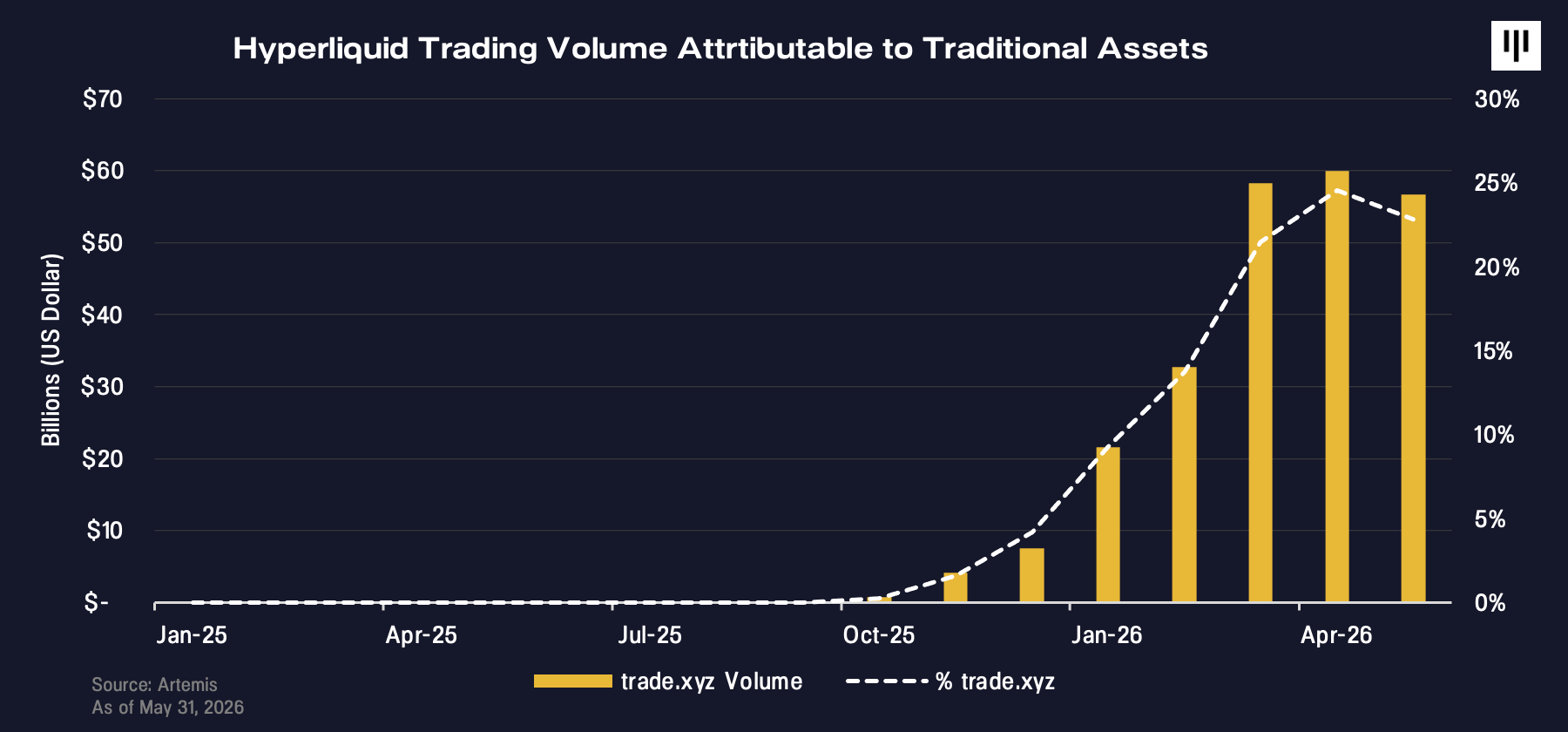

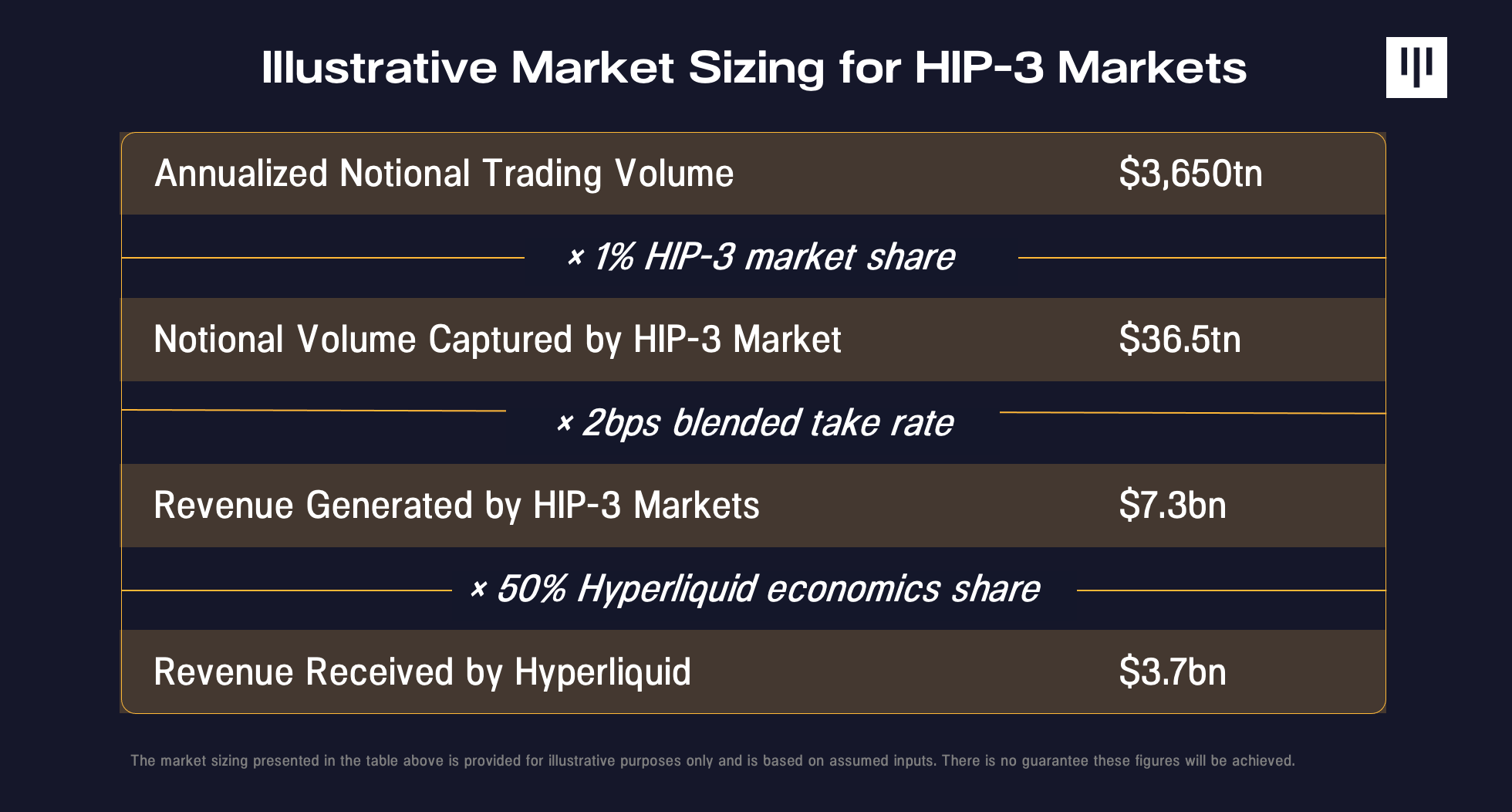

Hyperliquid has two properties native to blockchain that have helped it succeed in expanding its aperture to traditional assets typically traded on legacy exchanges. The first is that, as a decentralized exchange, Hyperliquid is open 24/7 by default, including on weekends and holidays. This compares to traditional exchanges like NYSE or CME which are only open five workdays a week. The second property is that Hyperliquid is permissionless, meaning any third-party can quickly list the assets people want to trade the most. Listed markets aren’t restricted to the imagination of the original Hyperliquid core team. Permissionless listings were unlocked by Hyperliquid Improvement Proposal 3 (HIP-3), which is a framework that allows any third party to permissionlessly list new perps markets and incentivize them with a share of transaction fees. An independent group operating under the trade.xyz brand has been the most prolific deployer.

As a result, the Hyperliquid platform has been able to adapt quickly to attract volume in whatever is the most topical asset at the time, including when traditional markets are closed, and the results have been striking. On-chain perps are becoming a parallel, always-on derivatives venue that is starting to meaningfully compete with traditional infrastructure. The clearest evidence is during moments of stress outside traditional trading hours. When gold and silver prices took off late 2025, Hyperliquid was the only venue on which it was tradeable on the weekends including that moment when China announced collateral requirement changes on silver trading. Silver briefly hit 2% of global derivatives volume at peak. When the Iran conflict started on a Saturday morning at the end of February, Hyperliquid was the only venue on which people could trade oil that weekend and daily crude volume surged to $3.7B. When oil futures opened Sunday night, they opened at the price oil perps were trading at already on Hyperliquid. Oil trading has reached 2% of global oil derivatives volume at peak. A month later, a fully licensed S&P 500 perp crossed $100M in volume on its first day. Traditional assets have at times reached as much as 40% of Hyperliquid’s volume, from essentially zero in late 2025.

Mainstream is Now Paying Attention

Hyperliquid’s traction has gained mainstream awareness this year. We are hearing more traditional asset hedge funds referencing Hyperliquid prices and even consider trading on the venue in order to be able to react to world events in a timelier manner.

Hyperliquid is becoming the exchange on which price discovery happens when all other markets are closed. Increasingly, this doesn’t just mean weekends, but also private companies prior to an IPO. On the day of Cerebras’ IPO (the largest IPO year-to-date), the banks underwriting the IPO were monitoring prices on Hyperliquid. A picture circulated showing Hyperliquid’s trading interface on a banker’s screen prior to the opening trade, [6]

Wall Street exchange incumbents are paying attention as well. On May 27 at Bernstein’s Strategic Decisions Conference, Jeffrey Sprecher, founder and CEO of Intercontinental Exchange, called Hyperliquid “bigger than Nasdaq” and noted that ICE had met its founders several times. Just two weeks prior, it was reported that ICE and CME were pressing regulators to rein in Hyperliquid[7], a sign they view this as a real competitive threat. The significance is that one of the world’s major exchange operators is now openly acknowledging Hyperliquid as a serious competitive challenge rather than a fringe experiment.

Interest is showing up in public equities, too. Hyperliquid Strategies Inc. (NASDAQ: PURR), the digital-asset treasury (“DAT”) dedicated to Hyperliquid that Pantera was an anchor investor in, holds HYPE on its balance sheet and is chaired by Bob Diamond, former CEO of Barclays, with David Schamis as CEO. The two have taken the case for HYPE directly to mainstream U.S. financial media, including on CNBC’s Squawk Box[8] and Bloomberg[9], bringing a traditional-finance pedigree and credibility to a crypto-native asset to spread awareness. PURR has traded up over 200% year-to-date as of June 1, 2026 and is one of the few DATs sustainably trading at a premium to NAV, implying strong demand.

The next catalyst to watch is the SpaceX IPO, reportedly targeting later this month. There is a SpaceX perp on Hyperliquid, giving traders a way to express a view on where the company will price before it becomes available to public equity investors on NASDAQ. SpaceX is currently trading around $200 per share[10] as of June 1, 2026 on Hyperliquid, or above where bankers are rumored to want to price the stock. Every market participant is watching this IPO and it’s reasonable to expect that Elon Musk, SpaceX’s well-known terminally online and crypto-supporter CEO, may push both bankers and prospective investors to consider where SpaceX is trading on Hyperliquid, in turn driving a step function increase in awareness for the platform.

How Big Could This Get

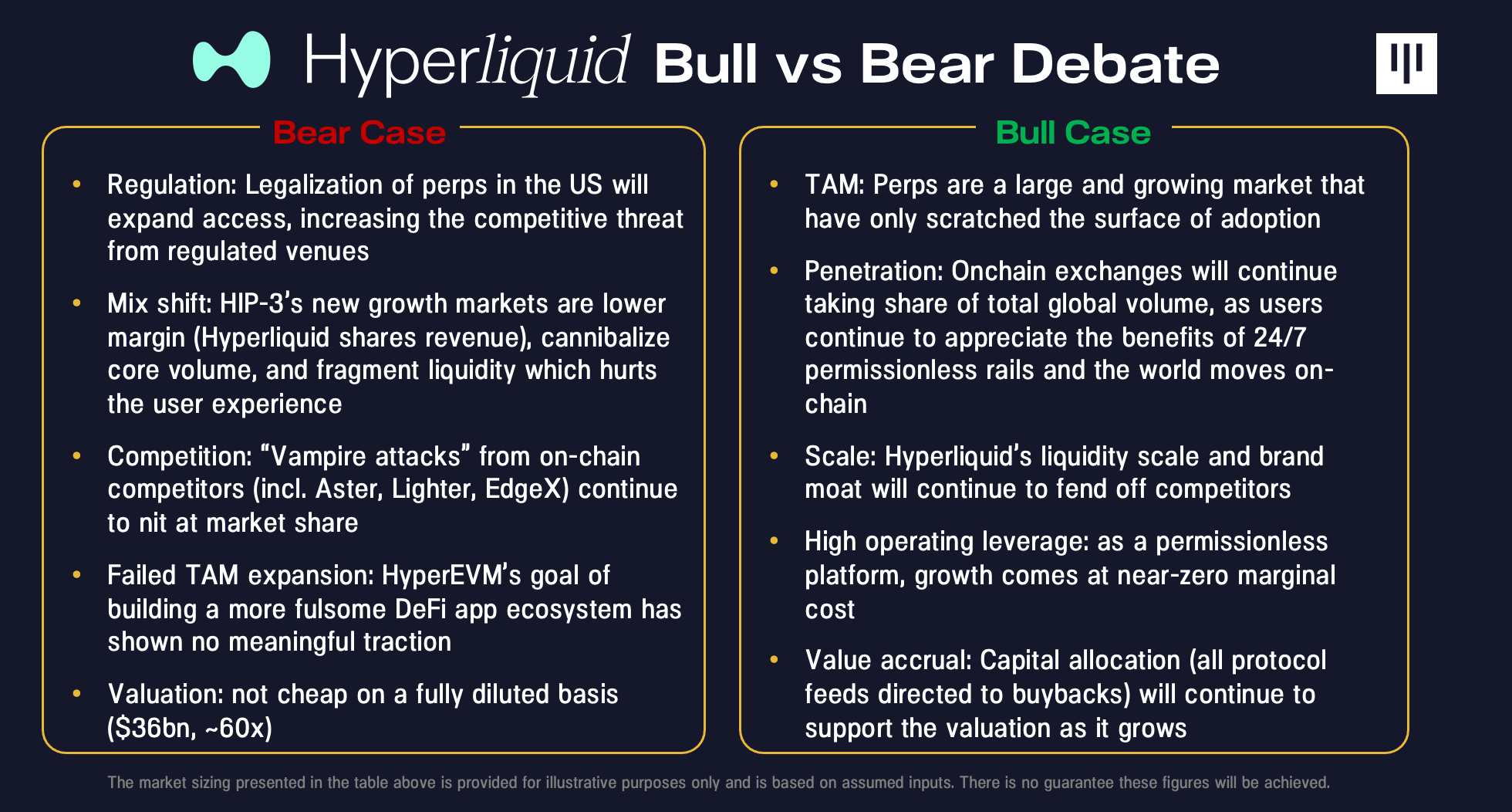

Hyperliquid is an onchain protocol whose capital structure is token-based. HYPE is the native token through which Hyperliquid’s protocol economics accrue value, most visibly through the platform’s programmatic buyback mechanism using 99% of revenues – a capital allocation policy similar to many fundamentally valuable stocks. The investment case for Hyperliquid is premised on a few pillars:

- ■ Massive and Growing Target Market: Hyperliquid is a disruptive platform targeting an attractive, expanding end market. Perpetual contracts (perps) are an innovative product that serves large swaths of investors better than traditional derivatives, historically monetizing at highly attractive transaction fees. As Hyperliquid expands from crypto-native markets toward its goal of “Housing All of Finance,” its total addressable market multiplies.

- ■ Strong and Execution and Scale Flywheel: The protocol has captured significant market share by scaling faster and more successfully than prior iterations of decentralized perp exchanges. In this market, scale creates a flywheel advantage: higher volume drives order book liquidity, which continually improves the user experience and attracts more capital.

- ■ Superior Product Experience: Hyperliquid delivers premium user experience by operating on its own custom Layer 1 blockchain built specifically for derivatives trading. User feedback has consistently highlighted that the platform vastly outperforms other decentralized exchanges and directly rivals the speed and UX of major centralized exchanges.

- ■ Direct and Powerful Value Accrual to Tokenholders: Crucially, these strong fundamentals translate directly into protocol profitability and token value. Hyperliquid generates $800M in annualized revenue[11], nearly all of which is funneled into its programmatic token buyback mechanism. This creates an uncommonly tight alignment between protocol growth and tokenholder value.

Zooming out, Hyperliquid’s TAM is on the order of $10T of daily notional trading volume. There is roughly $200B per day of equities volume in 0DTE options and leveraged ETFs, the current tools investors use for simple high-leverage directional exposure. Commodities derivatives trade $2T in daily volume, and Hyperliquid has shown it can make inroads especially on holidays and weekends. FX derivatives which trade roughly $8T per day and are almost entirely untapped on-chain, making them a big greenfield opportunity. Capturing even a low single-digit percentage of that combined volume sustainably implies a revenue potential 5x that of today, and presumably a similar valuation expansion potential.

That said, there are real risks to Hyperliquid as well and it is important to acknowledge that. The biggest risk to Hyperliquid is regulation. Perps are not currently freely available in the US, although there has been a move toward legalizing and listing them. Hyperliquid is a decentralized exchange which means it does not have KYC requirements, and while it geofences against US users it is not impossible to think there are workarounds. If perps are legalized in the US, the competitive set gets more serious for Hyperliquid and it could possibly lose volume share from US users moving to a regulated venue. One mitigant is that it’s also possible Hyperliquid launches a US regulated instance of the exchange, as others have.

Regulatory Developments: The Door Opens

The single largest constraint on the growth of perps in the U.S. has been regulatory, and it is the same uncertainty that pushed Hyperliquid’s team offshore to Singapore. True perpetual futures have not been available to U.S. persons, and both centralized and decentralized venues geofence American users.

That began to change last week. The CFTC approved a bitcoin-referenced perpetual futures contract submitted by Kalshi’s US registered exchange, and its staff separately cleared the way for Coinbase to offer certain crypto perpetuals through a foreign affiliate, treating them as foreign futures. The throughline is that the CFTC has opened a path for regulated crypto perps under existing futures frameworks, rather than demanding entirely new rulemaking. Some policy advocates believe that the historical absence of perps in the U.S. was less a deliberate regulatory choice than a commercial accident of which products incumbents chose to list, and that there was never a fundamental reason the CFTC could not permit them. The CFTC would just have to move now to make that clear if and when exchanges apply for more perps listings.

The harder question is what it takes to bring decentralized perps to U.S. users, and here the path is less clear. A centralized actor can register as a U.S. exchange today, and we have seen that others like Coinbase and Kalshi want to list real perps. For a permissionless onchain protocol, the Commission would need to extend exemptions, both from the requirement that derivatives trade on a registered exchange and from the rules on who may access certain contracts. The SEC and CFTC both have a pro-innovation stance and have previously made statements that support the idea that nothing in an onchain protocol’s core stack inherently requires registration. However, preserving permissionlessness and the absence of KYC while satisfying legitimate concerns around sanctions and market integrity will take some work to figure out.

Perps began at crypto’s edge because that was where market structure could evolve fastest. Perps are now moving toward the center of global finance. The recent CFTC actions do not resolve every regulatory question, especially for permissionless onchain venues, but they do mark an important shift. The U.S. is beginning to accommodate the product rather than dismiss it. Hyperliquid sits at the center of that transition. It has paired the best attributes of DeFi, which are open access, 24/7 markets, transparent settlement, and unusually strong stakeholder alignment, with a product that increasingly looks better suited to modern trading than the instruments it competes with. The question is no longer whether perps can matter outside crypto; the market is already answering that. The question is whether the infrastructure that the blockchain industry built first can become the place where the rest of finance increasingly prices risk, trades, and discovers.

![]()

TOKENIZED STARTUPS – RESTORING ACCESS TO PRE-IPO COMPANIES

Jay Yu, Junior Partner

Public markets for the world’s fastest-growing tech companies don’t work like they used to. 30 years ago, Amazon went public at a $438 million valuation, three years after its founding. Netscape IPO’ed eighteen months after it was created. But today, the fastest-growing companies – Stripe, SpaceX, OpenAI, Ramp – routinely stay private for a decade or more. The exposure to a company’s highest-velocity growth years, once accessible to public investors, has been quietly hijacked by private capital at ever-higher paper marks.

“If I were using cynical words, I’d say [venture capital] hijacked the growth years of early IPO companies. Amazon went public below a billion in market cap. It’s hard to fathom that today.” – Bill Gurley [12]

The market has responded with ad-hoc fixes: SPVs, secondary platforms, tender offers, and other instruments designed to quench investor thirst for growth-stage venture assets. But these are patches, not solutions. What investors may really want is what tech IPOs used to promise thirty years ago: broad, liquid exposure to generational companies with venture-scale upside.

Tokenized venture assets could be part of the answer. This piece explores how tokenized startups might bring these disjointed markets back into equilibrium across three questions: (1) why now is the right time for tokenized startups, (2) what does the landscape for tokenized startups look like, (3) what are the key opportunities, challenges, and unresolved tensions standing between this category and scale.

Part I – Why Now for Tokenized Startups?

Tokenized startups sit at the crossroads of three converging trends: (1) the explosion of ad-hoc instruments like SPVs as the de facto liquidity mechanism for generational tech companies, (2) the rapid growth of tokenized real world assets (RWAs), spanning money markets to public equities to commodities and more, (3) the breakdown of the “token-equity” consensus, where project tokens have increasingly become second class citizens relative to venture equity exposure.

1.1 – The Rise of SPVs

A decade ago, SPVs were a niche instrument – a way to pool capital outside of traditional venture or public financing structures [13]. But over the last two years, they’ve become a critical part of capital strategy, with platforms like AngelList, Carta, and Assure making it easier than ever to spin up SPVs for specific opportunities and companies [13]. In particular, secondary SPVs have grown by over 545% over the last two years, with more than a 10x in capital raised [14]. These ad-hoc market structures have captured significant market growth – Hiive’s weighted basket of the Top 50 secondary assets have seen a 49.1% growth in 2025, significantly outperforming the S&P 500 [15]. It is a sign that investors are using ad hoc private-market structures to recover functions that public markets used to perform more cleanly: access, liquidity, and price discovery. As companies stay private longer, SPVs have become one of the main substitutes.

1.2 – RWAs, Tokenization, and Perpification of Everything

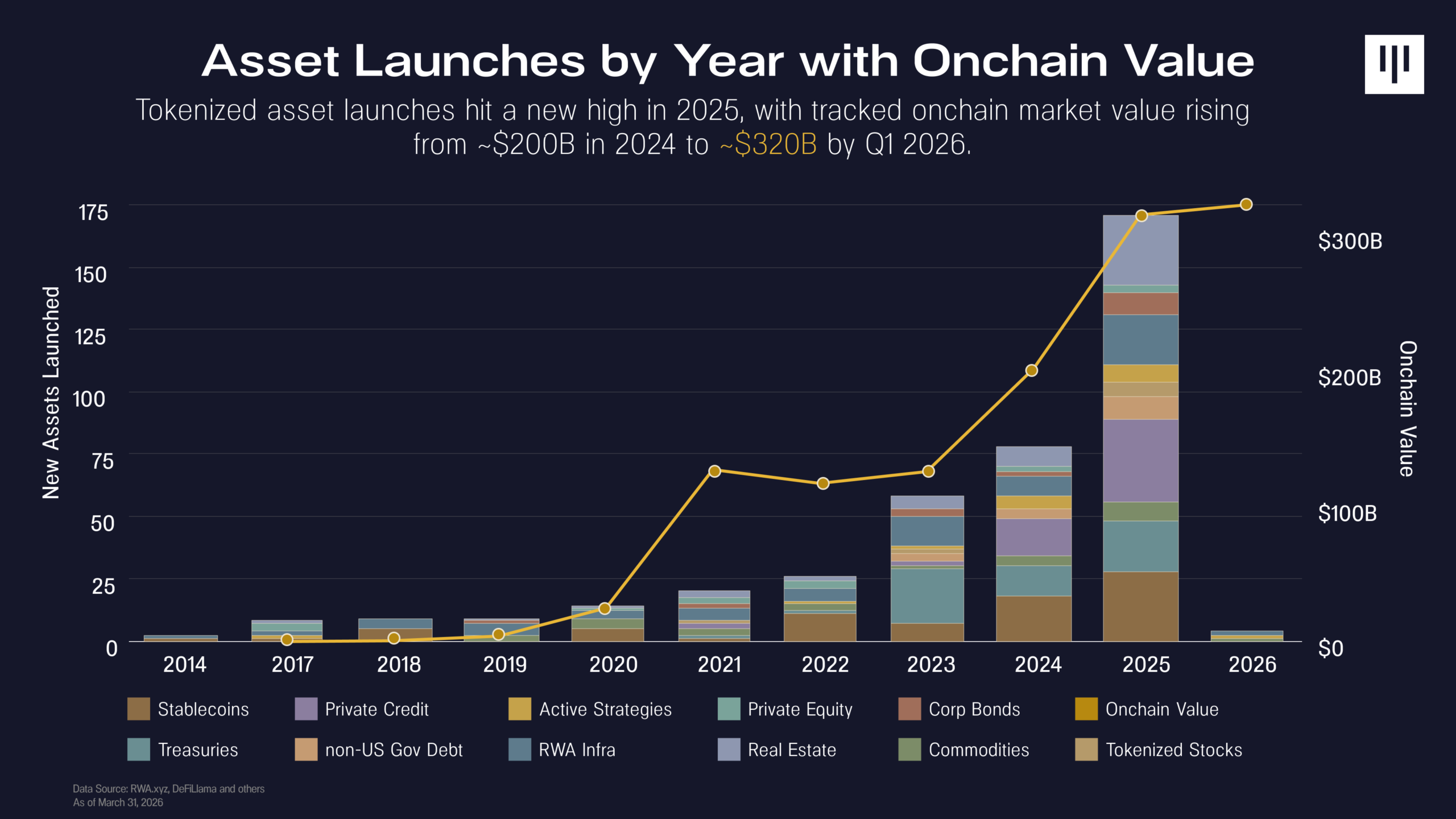

State of Tokenization Q1 2026 Report :: Pantera Research Lab

The second trend is the rise of tokenization and perpetual markets across a variety of asset classes. In Q1 2026, onchain RWA value has reached ~$320B [16]. While the largest RWA asset class continues to be US Treasuries (which can act as collateral for stablecoins), there has also been a significant rise in asset classes like commodities, stocks, and asset-backed credit like Figure’s home equity loans (HELOCs) [17]. As RWAs gain adoption, we can see the tokenization supply chain mature – from issuers to custodians to regulatory frameworks.

In parallel, perpetual futures, or “perps” have grown tremendously over the past 2 years, with the rise of perpetual decentralized exchanges (perp-DEXes) like Hyperliquid. Compared to dated derivatives, perps do not have expiry dates, which allow for better practical execution perspective, simpler to understand from a risk perspective, and natively 24/7 [18]. Projects like TradeXYZ have also expanded perps beyond pure crypto pairs (such as BTC-USDC) to other asset classes, including US and Korean stocks, commodities, and equity indices by offering a standardized way to create new perpetual markets in conjunction with HIP-3 [19].

1.3 – The Breakdown of the Token-Equity Consensus

The third growing trend is the value-accrual dilemma between tokens and equities. DeFi project tokens, such as UNI and AAVE were issued to explicitly not represent equity to address regulatory concerns. This created a “token-equity consensus,” where project tokens were supposed to be synthetic instruments giving owners “governance rights” over parts of a protocol, with fee collecting promises as a means to accrue value. However, this created a two-tiered system, with zero-sum value accrual, and tokenholders became like second class citizens to equity holders. This problem became clear with recent events like the Aave DAO vs. Labs standoff and the contentious Circle-Axelar acquisition, where tokenholders interests’ were subsumed to equity interests. All this prompts a rethinking of the existing “token-equity consensus” – how can we design tokens that better represent a project’s upside?

The convergence of these three major trends may pave the way for the rise of “tokenized startups”: tokenized exposure to a company with venture-scale upside, allowing the general public early access to generational companies the way the public markets used to. In this way, tokens become a re-architecturing of the traditional IPO, allowing broader public access to the hottest generational companies.

Part II – The Landscape of Tokenized Startups

2.1 – Design Approaches and Volumes Today

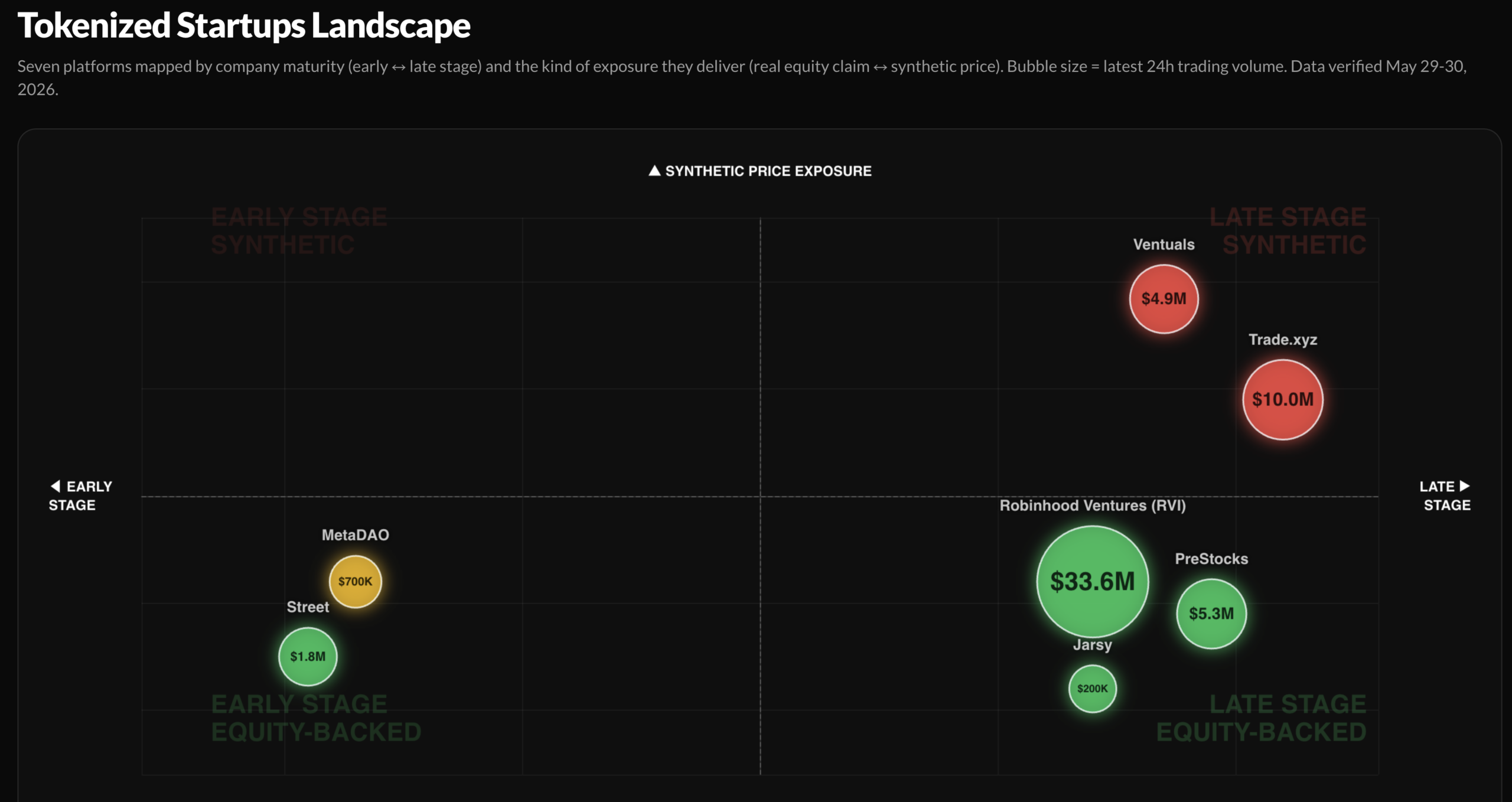

Landscape of Tokenized Startups. Made with Surf AI.

Today, there are a variety of approaches and designs to tokenized startups along two main dimensions – exposure mechanism, and startup stage. The exposure mechanisms of tokenized startups ranges from an equity-holding SPV instrument (such as PreStocks), to Closed End Funds with company equity access (such as Robinhood Ventures), to pure perpetual futures that provide only price exposure with no underlying equity ownership (such as TradeXYZ and Ventuals). The startup stages range from early-stage companies (such as MetaDAO’s platform) to growth stage assets and household pre-IPO names such as SpaceX, Anthropic, and OpenAI.

Mapping out the major players in the space and their scale (24hr trading volumes as of May 30), we notice several distinct patterns. Firstly, the biggest trend is that late-stage (esp. Pre-IPO startups) dominate early stage platforms by over 10x. In particular, users seem to gravitate towards exposure to Pre-IPO names, such as SpaceX, Anthropic, Anduril, and OpenAI, regardless of the platform offering these assets.

Secondly, equity-based tokenized startups, (such as via Robinhood Ventures and PreStocks) generally see more trading volume than their perps counterparts. Part of this could be simply skewed by Robinhood’s distribution as a platform, as well as TradeXYZ’s one-startup-at-a-time rollout of IPO perps. Notably, TradeXYZ’s IPO perpetual for Cerebras Systems was extremely successful, seeing over $30 million in daily volume and offering accurate price discovery within < 3% of the IPO price [20].

Thirdly, all platforms within this landscape see a power-law concentration effect, where the platform’s volume gets dominated by < 3 assets. MetaDAO, for example, has its trading volume dominated by META, Avici, and Umbra. Street has its volume dominated by KLED. TradeXYZ currently (as of May 30, 2026) only offers SpaceX via SPCX-USDC, and SpaceX also contributes to about half of PreStock’s weekly volume. This massive power law effect could indicate that for most platforms, traders are much more loyal to the brand-name high quality assets rather than the underlying platform itself.

2.2 – Project Design Architectures

We can also dive deeper to examine the individual projects within this landscape map more carefully to understand the various design tradeoffs in this space, ranging from perp exposure to SPV backed equities.

|

Platform |

Mechanism |

Representative Assets & Stage |

Strengths |

Weaknesses |

|

Perpetual futures on private company valuations via Hyperliquid HIP-3. Price = valuation / 1B. No underlying asset held. |

Late-stage only. vOAI, vSPX – any large private company by valuation signal. Pricing model requires well-known public valuation figures; illiquid early-stage companies have no oracle. |

No KYC or accredited investor requirement. Instant listings on any private company. No cap table friction. |

Zero asset backing. Oracle risk: prices derived from unaudited valuation rumors. No redemption mechanism. Testnet-only as of early 2026. Maximum regulatory exposure. |

|

|

Cash-settled perpetuals referencing anticipated public share price (not market cap). Each contract has an Outside Launch Date and a 60-day Settlement Period, then converts to a standard externally-priced perp once the company lists and oracle pricing is available. |

Late-stage / imminently pre-IPO only. First launch was CBRS (Cerebras), which saw $30M+ daily volume and priced within <3% of the actual IPO. Pipeline targets filed-S-1 companies. Currently only offers SpaceX via SPCX-USDC |

Cleanest price discovery observed in the landscape — CBRS tracked the IPO within 3%. Self-terminating structure resolves cleanly into post-IPO perps. Permissionless, no SPV or cap-table friction. |

Explicitly not equity — no ownership, voting, or dividend rights. Narrow window of applicability (only companies near IPO). One-asset-at-a-time rollout caps platform scale. Oracle and settlement risk during the pre-listing window. |

|

|

NYSE-listed closed-end fund (debuted March 2026, ~$1B target). Fund acquires direct equity in private “Frontier Companies”; retail trades RVI shares on the open market at ~$25/share. No accreditation, no performance fees. |

Late-stage only. Stripe, ElevenLabs, Databricks, Ramp, Airwallex, Revolut, Mercor, Oura, Boom — concentrated in household pre-IPO names. |

Real fund-level equity ownership inside a regulated, SEC-registered wrapper. NYSE listing provides genuine secondary liquidity and price transparency. Robinhood’s distribution drives retail access at scale. No accreditation requirement. |

Closed-end fund discount/premium dynamics decouple share price from NAV. Retail has a claim only on the fund vehicle, not on underlying shares. Concentrated portfolio at manager discretion. Fully off-chain — no tokenization or composability. |

|

|

SEC-registered closed-end fund managed by AngelList Asset Management. Pools retail capital across three sleeves: emerging fund managers, growth rounds, and secondary equity. Flat 1% management fee, no performance fees. $500 minimum. |

Late-stage only. xAI, Anthropic, OpenAI, Sierra, Vercel, Crusoe, Legora — concentrated in highest-demand AI names. |

Regulated SEC-registered structure with the lowest accessible minimum ($500) on the late-stage side. Naval-led oversight and AngelList deal pipeline. Diversified across primaries, secondaries, and sub-funds rather than single-asset exposure. |

No exchange listing — liquidity only via discretionary quarterly tender offers capped at 5% of NAV. Closed-end illiquidity with no continuous secondary market. Fund-level rather than asset-level exposure. Not tokenized; no onchain composability. |

|

|

Unruggable ICO launchpad + futarchy governance. IP and funds transferred to DAO LLC. Treasury locked; spending requires on-chain approval via decision markets. |

Early-stage only. Umbra, MtnDAO — crypto-native projects at inception. Not a secondary market vehicle. |

Strongest investor protection of any platform – funds structurally cannot be rugged. Legal wrapper via DAO LLC. $17.6M raised across 7 ICOs (Nov 2025). |

Scoped to crypto-native projects only. Mixed post-ICO performance (Trove -90%). Retail patience mismatch with ICO lockups. |

|

|

Accelerator + tokenization framework using ERC-S standard, routing economic upside to holders without triggering Howey. Issuer-initiated; founders tokenize a float starting at 1% with cap-table linkage. |

Early-stage only. First cohort at $40M valuation; pipeline toward $200M in equity commitments. Accelerator model targets companies at formation or seed, not unicorns. |

Only platform where the issuing company is the participant — alignment by design. ERC-S is a genuine attempt at a non-security legal framework. Tokenization doubles as distribution. Gradual float expansion preserves founder control. |

ERC-S non-security claim is entirely untested by regulators. Howey avoidance is a legal theory, not established precedent. Early-stage focus misses highest-demand assets (OpenAI, Stripe). Accelerator model limits scale. |

|

|

SPV acquires actual shares; tokens issued 1:1 representing proportional economic interest in SPV. Built on Solana (Jupiter + Meteora). $2.1M seed from Republic Capital. |

Late-stage only. OpenAI, Canva, SpaceX, Anthropic, xAI — ~22 unicorns with active secondary market demand. |

Genuinely backed by real shares. No minimum investment, no management fees, 24/7 trading. Solana infrastructure enables micro-fractional trades. Self-custody compatible. |

SPV complexity abstracted but not eliminated — ROFR, transfer restrictions, and cap table issues persist underneath. No detailed proof-of-reserve published. US and major jurisdictions excluded. No legal shareholder rights. |

|

|

Delaware LLCs acquire shares; tokens issued 1:1 tracking economic rights of underlying share. Proof-of-reserve publicly verifiable on-chain. Backed by Breyer Capital. Min. $10. |

Late-stage only. Anthropic, Stripe, SpaceX, Discord, Circle — established names with known secondaries. |

Public proof-of-reserve verifiable on-chain — strongest transparency of SPV-backed platforms. Delaware LLC structure adds legal clarity. $10 minimum. Breyer Capital backing. |

Same structural ceiling as PreStocks: SPV wrapper doesn’t dissolve underlying illiquidity or company ROFR. No voting or information rights. Liquidity dependent on platform-side market-making. |

Note: Platform comparisons and characterizations in this analysis represent the opinion of the author based on publicly available information as of 5/30/2026. Descriptions of platform strengths and weaknesses are not investment recommendations.

Part III – Challenges and Opportunities for Tokenized Startups

Tokenized startups are still in their infancy today, and the design space is filled with many opportunities and challenges [21].

3.1 – Equity Transfer Consent and Team Alignment

One of the most pressing questions right now for (spot-based) tokenized startup platforms is whether or not these projects actually work with or against the interest of the founding team of the company – especially as platform trading volumes are disproportionately concentrated 1-3 quality assets.

This is especially true for high-profile pre-IPO companies such as SpaceX, Anthropic, and OpenAI where much of the pre-IPO demand and volumes takes place. Without it, the company can publicly announce opposition to the tokenization, leading to sales being voided and subsequent crashes in token value, as seen with Anthropic opposing secondary SPVs and OpenAI opposing Robinhood’s stock tokens [23].

Generally speaking, growth-stage companies have four distinct incentives to pursue an IPO: (1) access to capital on public markets, (2) real-time pricing, (3) liquid exits for founding team and investors, and (4) prestige signalling.

Today, the proliferation of growth-stage “megafunds” provide the hottest startups with an extremely robust and plentiful funding environment – often at extremely generous valuations [22]. This dynamic diminishes incentives (1) and (2) for growth-stage companies to go public: they no longer need to turn to public markets for funding, and real-time pricing runs the risk of correcting prices downwards.

Thus, in today’s funding environment, a hot growth-stage startup will only go to public markets if there is a significant amount of early stage employees and investors wanting immediate liquidity (eg. Facebook’s 2012 IPO), or as a “coming-of-age” prestige badge.

For a spot-based tokenized startup platform to have board blessing for direct share access in the current funding environment, the latter two incentives carry much more weight. Traditional secondary brokers like Forge and Hiiv cater more to the liquidity incentive, whereas high-profile Closed-End Funds such as Robinhood Ventures and USVC arguably cater to the prestige incentive.

Nonetheless, in addition to these traditional IPO incentives, there is also a set of emerging designs, such as tokenized startup baskets, tokenized accelerator models, and tokenized community offerings that can solve this founder alignment problem:

- Tokenized startup baskets refer to tradable portfolios of growth-stage startups rather than single tokenized companies. This is the route that Closed-End Funds such as Robinhood Ventures offer. This mechanism could enable the liquidity and prestige, and potentially capital access incentives, while mitigating the downward-repricing pressure of the “real-time pricing” of public pricing by using a NAV multiple (somewhat similar to DATs).

- Tokenized accelerator models apply the traditional accelerator and incubation model (eg. YC, HF0, South Park Commons) in helping startups grow from 0 to 1 in exchange for their blessing to tokenize shares. We see launchpads such as Street and MetaDAO effectively offering this model – they solve the founder alignment issue by being on the founder’s side and actually helping the founders grow.

- Tokenized community offerings are perhaps the most interesting and exploratory model for tokenized startups. As shown during the Uniswap airdrop in 2020, tokens can act as great incentives for everyday users to use the product on a daily basis. When done well, a token airdrop reduces CAC by subsidizing organic user activity, boosting project marketing, and increasing user satisfaction, particularly for consumer-facing projects. Revolut, for example, did a community equity round that raised $1.3M from early users at a $40M valuation. This doubled as marketing, turned users into owners and evangelists, and those early backers have seen 400x returns. However, token airdrops can also be a double edged sword – many crypto project airdrops have been plagued by airdrop farming, accusations of insider allocations, and instant selling pressure.

3.2 – Non-US Jurisdictions

Another route around the founder alignment problem can just be to go global. Much of the current discussion around tokenized startups (and trading volumes) takes a US-centric approach, concerning the hottest US companies (such as SpaceX, Anthropic, OpenAI), and assuming a US IPO. But both the public and private capital markets in the US already serve growth-stage companies extremely well, which makes the additional benefits of tokenized offerings hard to justify for companies.

However, this is not necessarily true for other geographies, where the local capital markets may be inefficient and not provide the best liquidity or pricing for the fastest-growing companies. Wise, for example, originally listed on the London Stock Exchange in 2021. However, in May 2026, it shifted its primary listing to the US NASDAQ, as it believed the move could draw on more liquid markets, have broader access to both retail and institutions, and have a more generous valuation multiple [25].

This geographical divergence in valuations and capital access is also evident in the difference in valuation multiples between US AI companies and their Chinese counterparts. Whereas US AI leaders routinely have P/S ratios of 15-40x, Chinese AI companies see much more conservative ratios of closer to 5-15x. This discount may partially be attributable to capital access – the Chinese capital market is generally much harder to access than the US markets. This geographical valuation arbitrage becomes particularly interesting as different parts of frontier supply chains – such as for AI, robotics, semiconductors, biotech – remain spread across the world, with relevant companies listed across markets in Asia and Europe.

Yet, despite this structural advantage that non-US jurisdictions have in tokenized startups, currently there is limited empirical experiments and volumes, possibly due to the difficulty in sourcing high-demand startups willing to experiment with their cap table, as well as complications with local regulations around foreign investments and tokenization. A particularly interesting non-US market to watch for tokenized startups is South Korea. South Korea has (1) several national champions such as Samsung and SK Hynix in the AI supply chain with global investor demand, (2) a new legal framework for “stock tokens”, (3) brokerages actively paying attention to pre-IPO investments, and (4) more crypto investors than stock investors. Indeed, this may be part of the reason why projects like TradeXYZ actively started to list perpetuals on Korean stocks.

One of tokenization’s greatest strengths is in its geographical arbitrage capability, able to provide a global audience ground-floor access to companies from all over the world. Tokenized startup platforms – with their global liquidity base and potential accessibility to a broader set of retail and institutional investors could very well become part of the uplisting strategy of the next generation of the Wise’s of the world – fast growing companies outside of the US that do not have as robust local capital markets.

3.3 – Price Discovery Design for Perps

The other route for tokenized startup platforms is the perp playbook. If all you have are synthetic instruments that do not represent underlying equity, then there is nothing a board can actually void. This sidesteps the need for team access and board consent. However, synthetics trade legality for a price discovery problem.

Existing perps markets – such as perps for crypto tokens, stocks, and commodities – typically assume a liquid spot market and reliable price oracle to manage funding rates and synthetic prices. However, private startups by definition do not have liquid public markets. The closest that you get are tender offers and secondary purchases, which platforms like Ventuals use to anchor their funding rates. However, these are often unreliable, and routinely underprice pre-IPO assets. On Ventuals, for example, the funding rate runs about 15% annualized within 5% of the oracle, and beyond that climbs an exponential curve, creating punitive fees for longs.

TradeXYZ takes an opposite approach, relying on an oracle-less price discovery. For the IPO for Cerebras Systems for example, TradeXYZ simply had a Hyperp mechanism deriving the reference from the market’s own recent marks, and let the contract discover price in the narrow window between the S-1 and the listing. It worked better than anything else in the market. Launched May 1 at a $175 reference, CBRS traded $288-320 for two weeks and printed around $340 an hour before the open, within 3% of the $350 at which Nasdaq actually opened [20]. This estimate was roughly 84% above the $185 the bankers priced, and far more accurate than secondary brokers like Hiive ($225) and Forge ($113.50). This was a tremendous triumph for the perp as an instrument.

However, this process is not necessarily scalable, as clean discovery depended on an imminent, verifiable convergence event. Had Cerebras not listed within a certain time period, the contract would have settled to a TWAP of its own price. In this sense, the “perp price discovery” mechanism ended up looking like more like a traditional futures contract, and is also not necessarily scalable to earlier stage pre-IPOs that may not IPO anytime soon.

Thus, the design space for perp-based tokenized startups remains wide open. The scalable formula is yet to be written, and is likely one that blends together crypto perps with traditional futures, prediction markets, secondary spot markets, contracts for differences (CFDs) amongst other primitives. With Kalshi’s recent entrance into the perpetuals markets, and Hyperliquid’s entrance into outcome markets with HIP-4, we’re seeing a great convergence between all of these different pricing instruments. The pricing of tokenized pre-IPO startups could very well be the catalyst case for a novel derivatives landscape – one that is more efficient and accessible to the everyday user.

3.4 – Legal Structure and Regulation

From a legal structure perspective, many of these tokenized startup instruments, such as Street’s ERC-S, MetaDAO’s DAO LLC, and SPV-backed tokens are novel and experimental, and have not really withstood the test of time with a regulator with strict enforcement intent. Even the recent US CLARITY Act that addresses digital commodities does not address this question of tokenized equity.

From public statements, the SEC seems to bucket these tokenized startups into two distinct categories depending on whether the tokens are directly issued by the company or by third parties [24].

Issuer-sponsored tokens are the security itself, just re-formatted, and therefore are subject to traditional securities laws. Whether the official ledger sits on-chain (moving the token moves the share) or off-chain (the token triggers a books update), the treatment is identical to an ordinary share: register or qualify for an exemption, and carry every standard disclosure and reporting obligation.

Third-party tokens are treated by what they actually convey. A custodial token is a security entitlement under UCC Article 8 – a real securities transaction, but a claim on custodial shares rather than the shares themselves, which means you also absorb the custodian’s insolvency risk. A synthetic token is a wholly separate security issued by the third party, conveying no rights against the referenced company and requiring its own registration or exemption: linked securities (a note or SPV tracking the target’s value) sit here, while security-based swaps, such as the Ventuals-style perp, are the most constrained, barred from ordinary US retail unless both registered and traded on a national exchange.

Conclusion

Whether it be pre-IPO perps or SPVs, closed-end funds or secondary tenders, each of these instruments is an attempt to win back what public markets used to give away freely: early, liquid exposure to companies in their highest-velocity years, rather than let it get captured by growth equity funds.

Today, we know that the demand exists, but the infrastructure is yet to catch up. And for tokens, the stakes run deeper. The last few years have been an identity crisis: project tokens drifted into second-class citizenship, governance theater stapled to value that accrued elsewhere. Reinventing the IPO – giving the token a real claim on venture-scale upside –may be the generational mission that absolves it, returning the token to its ICO-era promise with the infrastructure the first wave never had.

PANTERA CONFERENCE CALLS[C]

Our investment team hosts monthly conference calls to help educate the community on blockchain. The team discusses important developments that are happening within the industry and will often invite founders and CEOs of leading blockchain companies to participate in panel discussions. Below is a list of upcoming calls for which you can register via this link.

Liquid Token Fund Investor Call

Tuesday, July 7, 2026 12:00pm Eastern Daylight Time / 18:00 Central European Summer Time / 12:00am Singapore Standard Time

Open only to Limited Partners of the fund.

Pantera Growth Opportunities Fund Call

Our newest strategy targeting growth-stage blockchain companies on the path to public markets

Tuesday, July 14, 2026 12:00pm Eastern Daylight Time / 18:00 Central European Summer Time / 12:00am Singapore Standard Time

https://panteracapital.com/pantera-growth-opportunities-fund-july-2026/

Pantera Fund V Call

An overview of Pantera’s fifth venture-style fund that offers exposure to the full spectrum of blockchain assets

Tuesday, August 11, 2026 12:00pm Eastern Daylight Time / 18:00 Central European Summer Time / 12:00am Singapore Standard Time

https://panteracapital.com/aug-11-conference-call-fund-v/

Join us in learning more about the industry, the opportunities we see on the horizon, and our funds.

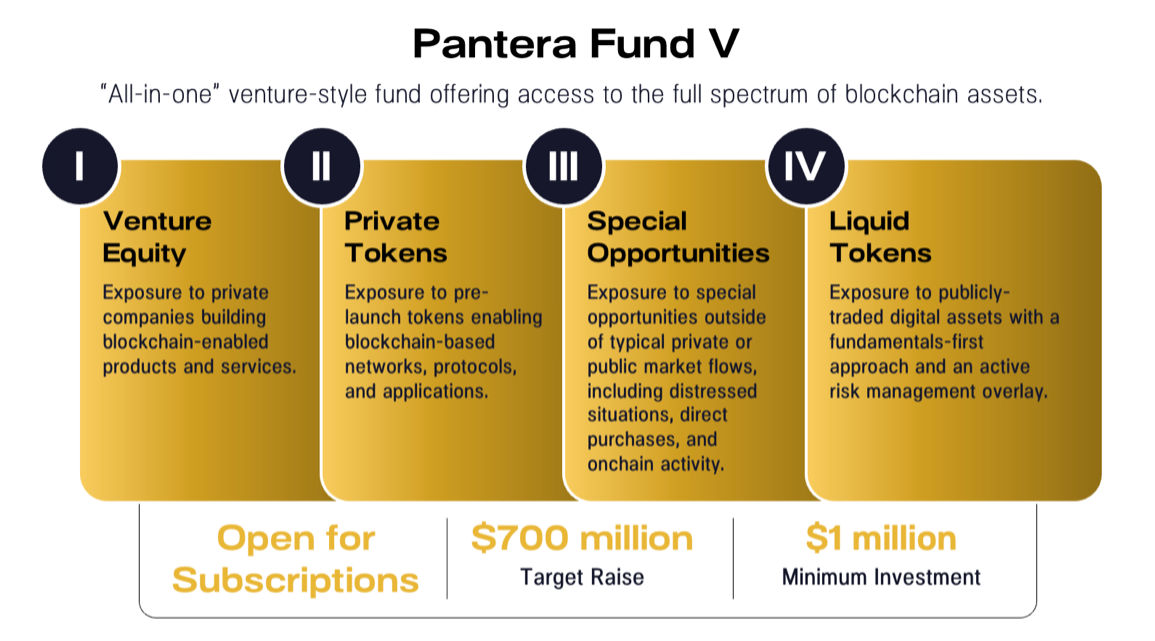

PANTERA FUND V

We’ve found that most investors view blockchain as an asset class and would prefer to have a manager allocate amongst the various asset types. This compelled us to create Pantera Blockchain Fund (IV) in 2021, a wrapper for the entire spectrum of blockchain assets. Its successor — Pantera Fund V — is now open for subscriptions.

Similar to its predecessor, we believe this new fund is the most efficient way to get exposure to blockchain as an asset class. It is a continuation of the strategies we have employed at Pantera for twelve years across twelve venture and hedge funds.

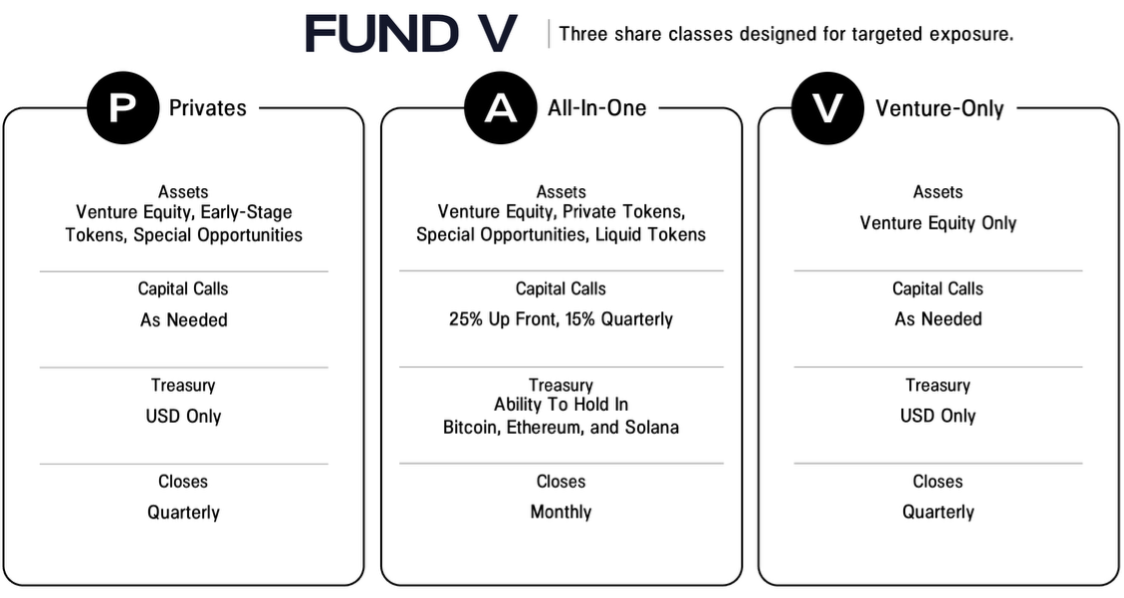

Limited Partners have the flexibility to invest in just venture (Class V for “Venture”), or in venture, private tokens, and locked-up treasury tokens (Class P for “Privates”), or the all-in-one Class A.[A],[B]

As in all previous Pantera venture funds, we strongly support helping our LPs get access to private deals in this fund. Fund LPs with capital commitments of $25mm or more will have the option to collectively co-invest in at least 10% of each venture equity, private token, and special opportunity deal that the Fund invests over $10mm in. There is no management fee or carried interest on co-investments for those with co-investment rights.

We will endeavor to offer co-investment opportunities, on a capacity available-basis, to other LPs as well. These co-investment opportunities are subject to 1/10% fees.

We are now accepting subscriptions for Fund V. If you’re ready to invest, please click the button below to begin the process.

If you are new to Fund V and would like to receive additional information, click here. We also invite you to join our next call on Pantera Fund V on Tuesday, August 11, at 12:00pm Eastern Time. You may register here.

Pantera donates 1% of revenue from all new funds to 1% For The Planet.

[A] Important Disclosures – This Section Discusses Pantera’s Advisory Services. Information contained in this section relates to Pantera’s investment advisory business. Nothing contained herein should be construed as a recommendation to invest in any security or to undertake an investment advisory relationship, or as any form of investment, legal, tax, or financial advice or recommendation. Prospective investors should consult their own advisors prior to making an investment decision. Pantera has no duty to update these materials or notify recipients of any changes.

[B] The above is presented for illustrative purposes only as a sample of potential opportunities Pantera could evaluate for Fund V and is not intended to limit Pantera’s investment activities in any way. There is no guarantee that similar opportunities will be available, or that Fund V will have similar investments to its predecessor fund.

[C] The terms summarized here are provided for informational purposes only and do not constitute a complete overview of the terms of Fund V. Terms are subject to further review and are qualified in their entirety by Fund V’s offering and governing documents.

References

[1] CryptoQuant, “FY 2025 Review of Crypto Exchange Activity”

[2] Coinglass, “2025 Annual Report”

[3] Artemis, TheBlock, Pantera analysis

[4] Blockworks Research, “Perp DEXs Analytics”

[5] Colossus, “Beyond the Sky: Jeffrey Yan & Hyperliquid” (April 2026)

[7] Bloomberg, “CME, ICE Push US to Curb Crypto’s Oil Trading Upstart”

[8] CNBC, “Sonnet-Hyperliquid Deal Approved, Merger Creates $1 Billion Crypto Treasury”

[9] Bloomberg, “More Real World Assets Are Coming On-Chain: Diamond”

[10] Hyperliquid, “SPCX Trading”

[11] Blockworks, Hyperliquid Annualized Revenue

[12] https://x.com/tbpn/status/2026417110025720048?s=20

[13] https://www.allocations.com/blog/what-is-an-spv-the-definitive-guide-to-special-purpose-vehicles

[14] https://venturesecondaries.substack.com/p/the-spv-race-why-pre-ipo-companies

[15] https://www.hiive.com/market-reports/state-of-the-pre-ipo-market-2026-annual-report

[16] https://panteracapital.com/state-of-tokenization-q1-2026-pdf/

[18] https://panteracapital.com/rise-of-perps-and-hyperliquid/

[20] https://x.com/ArrakisFinance/article/2055338763442934205

[21] https://x.com/DWFLabs/status/2060018127950500104?s=20

[22] https://blog.joinodin.com/p/the-magical-money-tree-of-management

[23] https://aurum.law/newsroom/Pre-IPO-Secondary-Tokenisation-After-Anthropic-and-OpenAI

[24] https://www.morganlewis.com/pubs/2026/02/sec-clarifies-federal-securities-law-treatment-of-tokenized-securities

[25] https://www.reuters.com/business/finance/wise-set-make-nasdaq-debut-company-completes-shift-london-new-york-2026-05-11/

This letter is an informational document that primarily provides educational content and general market commentary. Except for certain sections specifically marked in this letter, no statements included herein relate specifically to investment advisory services provided by Pantera Capital Partners LP or its affiliates (“Pantera”), nor does any content herein reflect or contain any offer of new or additional investment advisory services. Nothing contained herein constitutes an investment recommendation, investment advice, an offer to sell, or a solicitation to purchase, any securities in Funds managed by Pantera (the “Funds”) or any entity organized, controlled, or managed by Pantera and therefore may not be relied upon in connection with any offer or sale of securities. Any offer or solicitation may only be made pursuant to a confidential private offering memorandum (or similar document) which will only be provided to qualified offerees and should be carefully reviewed by any such offerees prior to investing.

This letter aims to summarize certain developments, articles, and/or media mentions with respect to Bitcoin and other cryptocurrencies that Pantera believes may be of interest. The views expressed in this letter are the subjective views of Pantera personnel, based on information that is believed to be reliable and has been obtained from sources believed to be reliable, but no representation or warranty is made, expressed, or implied, with respect to the fairness, correctness, accuracy, reasonableness, or completeness of the information and opinions. Analyses and opinions contained herein (including market commentary, statements or forecasts) reflect the authors’ judgment as of the date this letter was published, and may contain elements of subjectivity (including certain assumptions) or be based on incomplete information. The information contained in this letter is current as of the date indicated at the front of the letter. Pantera does not undertake to update the information contained herein.

This letter is not intended to provide, and should not be relied on for accounting, legal, or tax advice, or investment recommendations. Pantera and its principals have made investments in some of the instruments discussed in this communication and may in the future make additional investments in connection with such instruments without further notice.

Certain information contained in this letter constitutes “forward-looking statements” (including predictions), which can be identified by the use of forward-looking terminology such as “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue”, “believe”, or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual policies, procedures, and processes of Pantera and the performance of the Funds may differ materially from those reflected or contemplated in such forward-looking statements, and no undue reliance should be placed on these forward-looking statements, nor should the inclusion of these statements be regarded as Pantera’s representation that the Funds will achieve any strategy, objectives, or other plans. Past performance is not necessarily indicative of or a guarantee of future results. There is no guarantee that investments in any instrument or type of instrument described herein will be profitable – all investments carry the inherent risk of total loss.

It is strongly suggested that any prospective investor obtain independent advice in relation to any investment, financial, legal, tax, accounting, or regulatory issues discussed herein. Analyses and opinions contained herein may be based on assumptions that if altered can change the analyses or opinions expressed. Nothing contained herein shall constitute any representation or warranty as to future performance of any financial instrument, credit, currency rate, or other market or economic measure.