Housing All of Finance: The Rise of Perps and Hyperliquid

June 2, 2026 | Cosmo Jiang, Cody Poh

Housing All of Finance: The Rise of Perps and Hyperliquid

Perpetual futures, or “perps”, are on a path to becoming one of the dominant trading instruments in global financial markets. Perps are evolving from a crypto-native phenomenon to become a fundamental shift in market structure, and one that traditional investors can no longer ignore. The idea is not new. Its enabling infrastructure has now caught up, in particular onchain in decentralized finance, and as of last week, with a set of actions from the CFTC, the U.S. regulatory system has begun to formally accommodate it.

Perpetual Futures’ Advantages

The first formal futures market was the Dojima Rice Exchange, established in 1730 to facilitate Japanese rice farmers hedging crop price risk. Outside speculators realized they could trade those contracts to take directional bets on the price of rice, on margin with leverage and without taking physical delivery of rice (cash-settled). Capitalism played out as it does, and in due course today futures span all major asset classes (commodities, FX, equities), and the majority of futures trading relates to leveraged, directional bets.

A perpetual future is a futures contract that never expires. In place of an expiry, perps use a funding rate, a small periodic payment (e.g. 1-hour, or most frequently on crypto exchanges 8-hours) between longs and shorts: when the perp trades rich relative to spot, longs pay shorts, and when it trades cheap, shorts pay longs. Basis arbitrageurs step in to tether the contract price to spot. The lack of expiry is a simple-sounding design choice with meaningful benefits relative to existing derivatives (e.g. dated futures and options), including being easier to manage from a practical execution perspective, easier to understand from a risk perspective, and natively 24/7.

From a practical execution perspective, perpetual futures require less management than traditional futures. Traditional futures have expiry dates (e.g. monthly), which is why they’re also often called “dated-futures”. To hold a position over a longer period of time a trader must continuously roll from one contract to the next, sometimes managing a strip of multiple contract expiries each with their own basis between the future and spot. A perp collapses that complexity into one continuous position with no expiries and thus nothing to roll. A trader can hold for seconds or, in theory, forever without needing to worry about managing the trade.

From a risk management perspective, perps are also easier to understand than other derivatives. Dated futures require taking a view on a specific timeframe. With options, which also have a specific expiry, a trader can be right on direction but still lose to time decay or a shift in implied volatility. A perp strips away those complexities and allows a trader to express conviction more directly and nearly solely (although not entirely) on price.

Perps are also always on, trading 24/7 with no market hours and no weekend gaps. For an internet-native user base that lives in an always-on economy with global information connectivity, continuous access is not a feature. It is the expectation. Traditional exchanges are already moving in this direction at the behest of these market demands. Perps are the natural instrument to use if one fast forwards in its current direction.

Given its origins the dated-future is feeling, well, a bit dated. For the directional leveraged exposure most participants want, the perpetual future is a more natural instrument with all the benefits stated above.

Digital Assets Laid the Groundwork for Perpetual Futures

The design of the perpetual future is nothing new, dating back to a 1993 paper by Nobel laureate Robert Shiller. However, existing market structure in traditional exchanges created too much friction to allow it to catch on. Without the baggage of the legacy system and instead by being internet-native, the digital assets industry created the environment for perps to blossom. The detailed mechanics that made perps work were first solved at scale in 2016 to trade Bitcoin by BitMEX, which grew tremendously on the back of this innovation.

Perps have gone on to experience tremendous traction. In 2025, total perps trading volume on centralized exchanges was $62 trillion[1]. This is many multiples of spot volume of roughly $19 trillion and is the majority of the $86tn total derivatives trading volume[2], showing the market’s preference of perps over options.

For most of their history, perps were traded on centralized exchanges (CEX). The more interesting story recently has been the migration on-chain to decentralized exchanges (DEX). There have been many earlier attempts that found some level of success, with the most notable being GMX and Synthetix which used pool-based trading models and DYDX which used a central-limit order book and dedicated blockchain, but each struggled to match centralized venues on latency, liquidity and user experience.

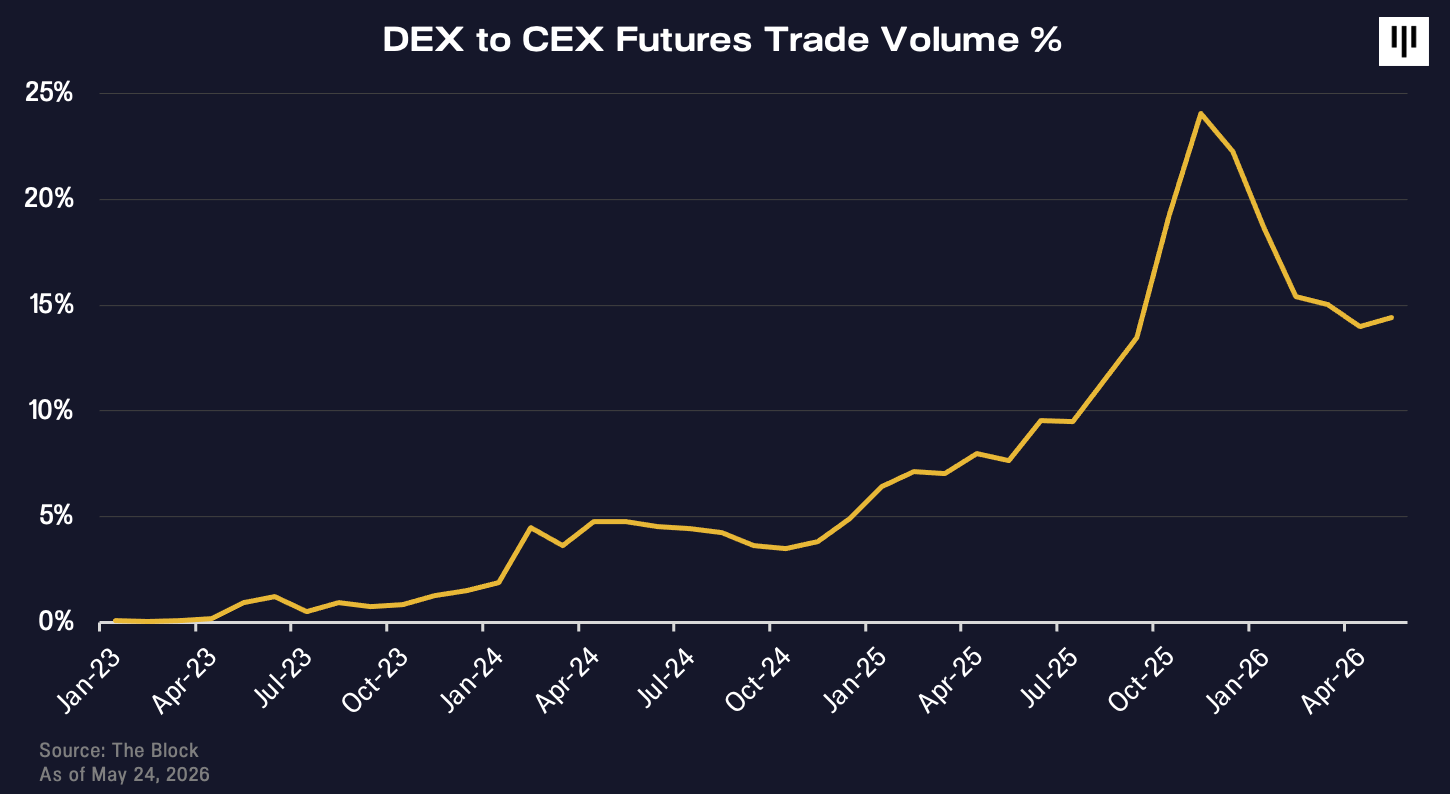

Hyperliquid has taken DEX perps to the next level, meaningfully increasing the market share of onchain perps. DEX perps volumes have reached 14% of CEX perps volumes, up from less than 1% in at the beginning of 2023 when Hyperliquid first launched.

The Rise of Hyperliquid

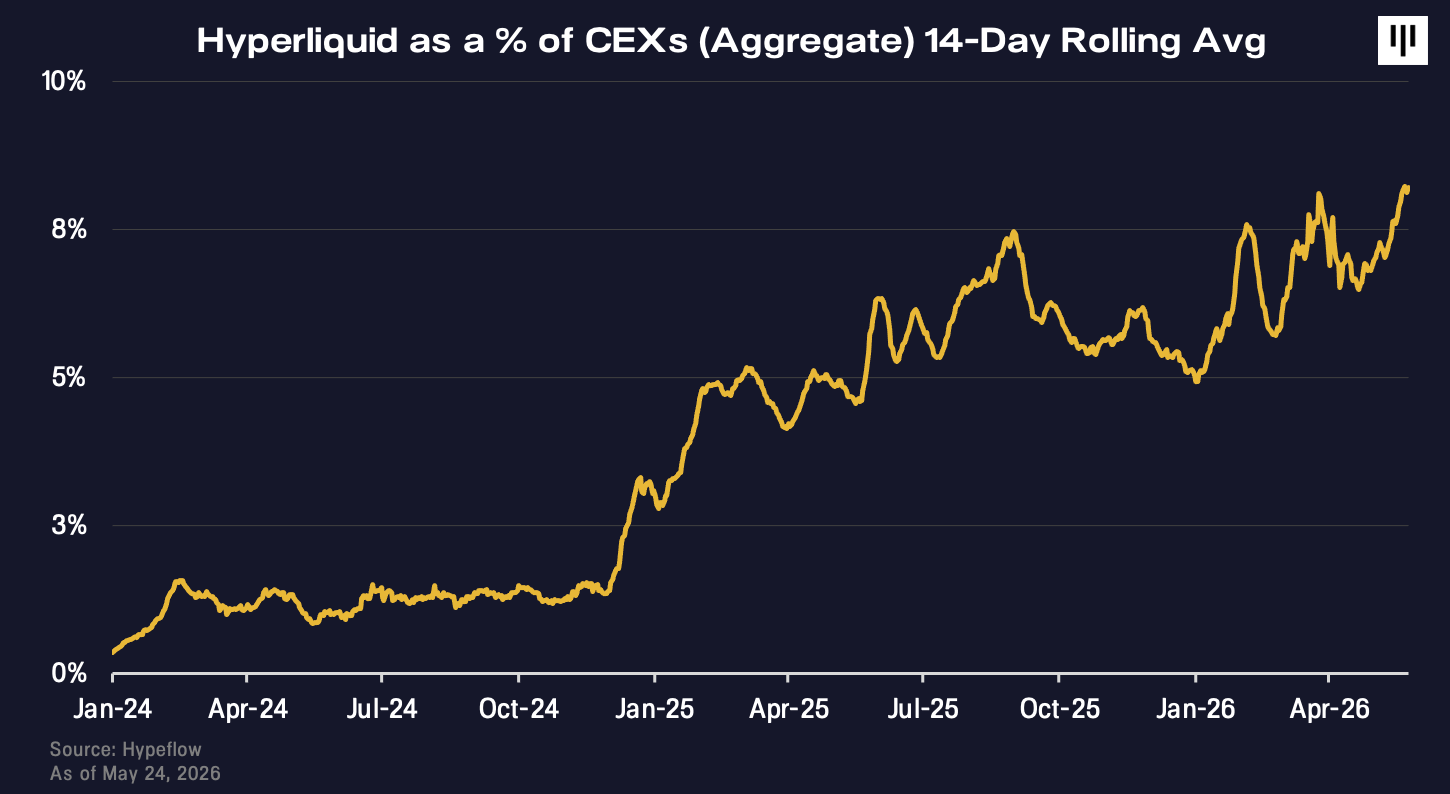

Hyperliquid is the largest decentralized perpetuals exchange, with roughly 40% of on-chain perp volume[4]. Hyperliquid was conceived of by Jeff Yan, a Harvard Math 55 alum and former high-frequency trader who had spent the prior years running an under-the-radar market-making firm, Chameleon Trading. The collapse of FTX was the catalyst for building Hyperliquid; Yan redirected his trading team’s efforts to instead create a decentralized alternative to the centralized exchanges that had just failed their users, acknowledging that existing blockchains were too slow for professional on-chain trading[5].

The team built its own Layer 1 blockchain purpose-built for trading and released it to the world at the end in February 2023. One of these changes included adding a speed-bump like feature that prevented the most aggressive high-frequency trading firms from taking advantage of market makers, hurting near-term transaction volume in favor of healthier growth. To address the cold-start problem that all exchanges face, the team bootstrapped liquidity by opening up their own proprietary trading algorithm for anyone to participate in via an onchain vault called HLP, the Hyperliquidity provider. Giving away this high-performance strategy to the public for free had the added benefit of winning the favor of the community, who became aligned advocates to further bolstering Hyperliquid’s growth. Worried about U.S. regulatory uncertainty regarding decentralized finance and perps, they also relocated to Singapore in Spring 2024, one of many major losses the US suffered as a result of its prior regulatory stance that is now being rectified.

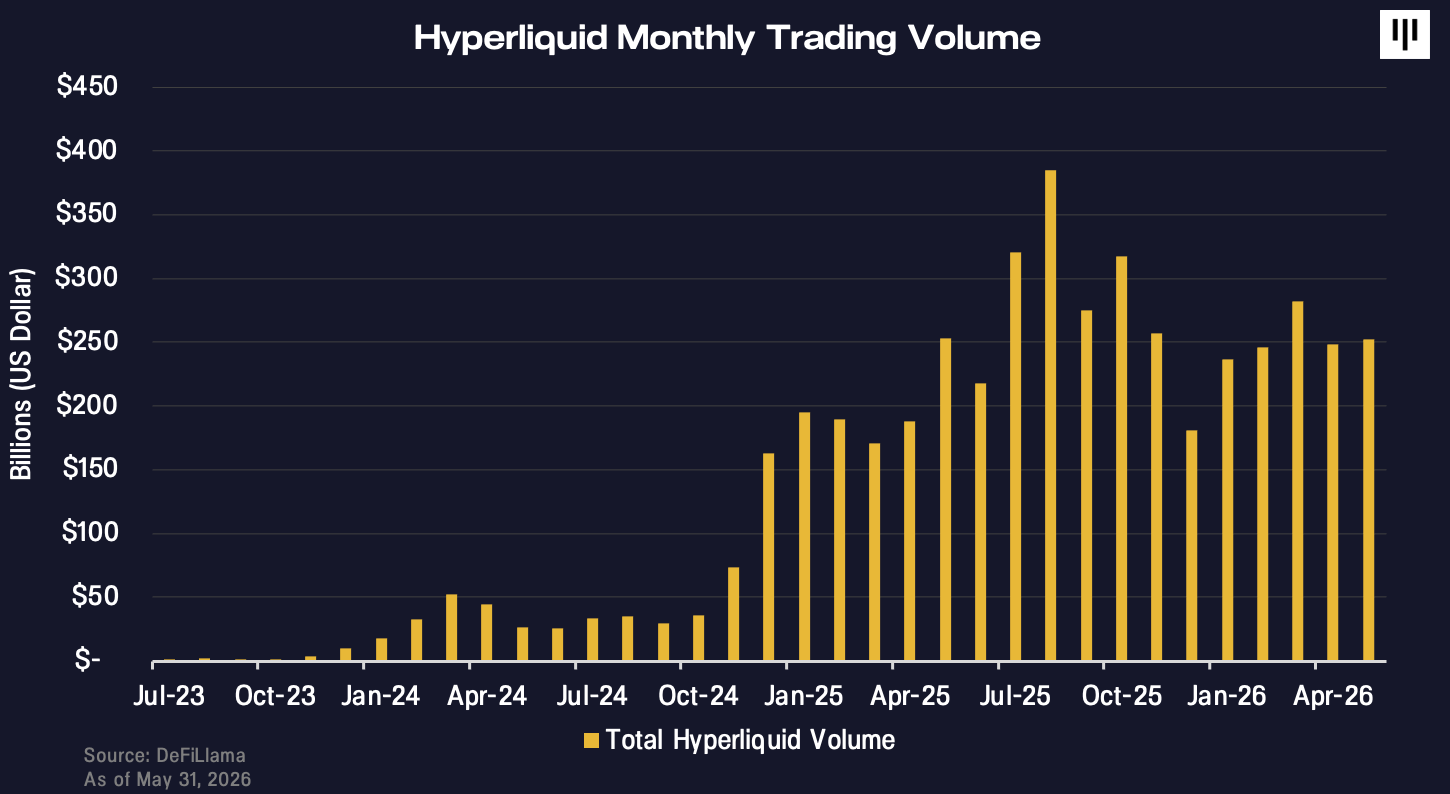

Through a combination of a high talent density core team, a stakeholder alignment ethos that represents the best of crypto’s ideals, and incredible execution Hyperliquid has outran its competition to now be the largest and most profitable decentralized perps exchange with over $250B monthly volume and $800M annualized revenue. Hyperliquid continues to grow trading volumes, over time taking an increasing relative share of volume vs centralized exchanges.

From Digital Assets to “Housing All of Finance”

Hyperliquid’s growth this year has accelerated as it expanded beyond crypto-native assets into equities, commodities, indices and private companies. Jeff Yan has described the vision “Housing All of Finance” on a single venue.

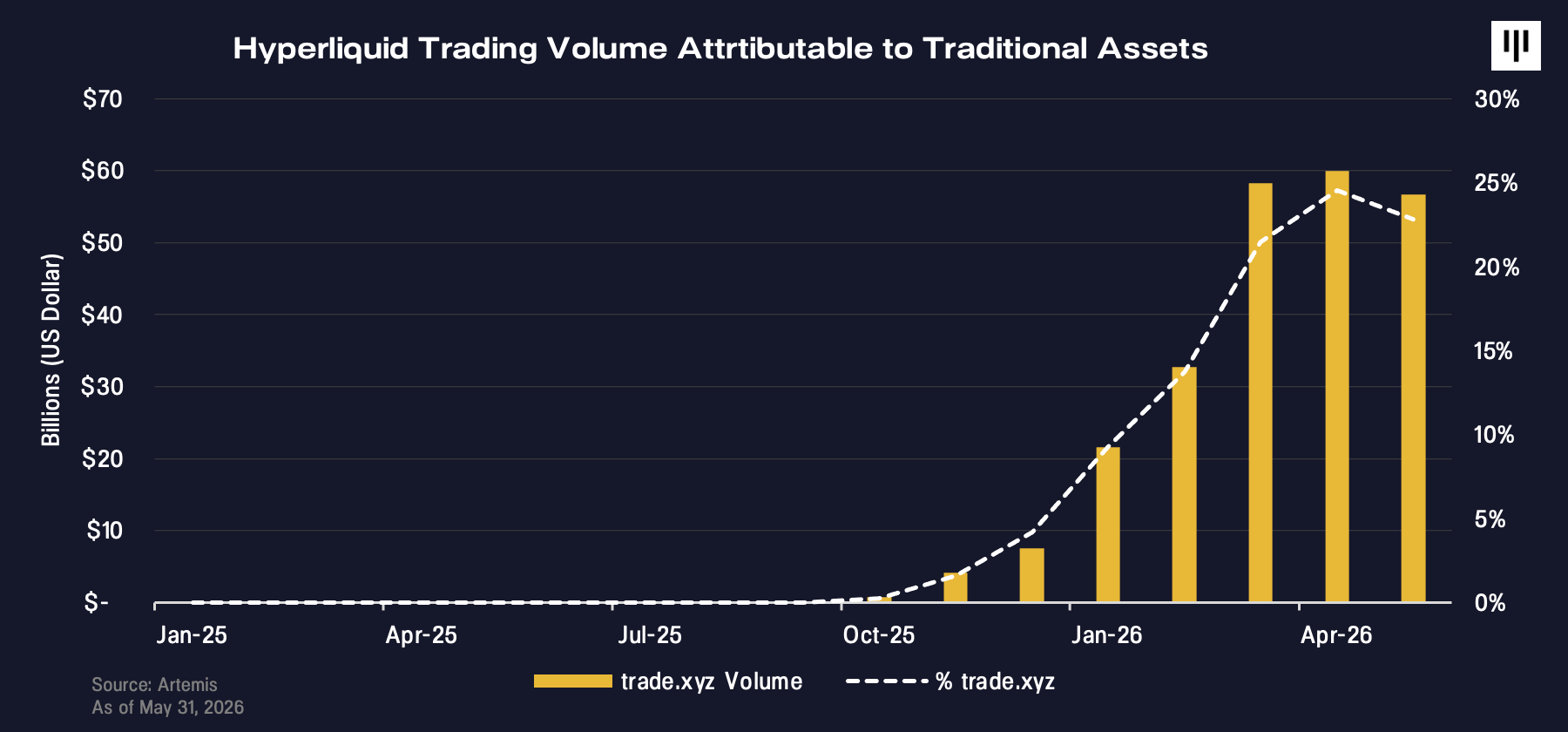

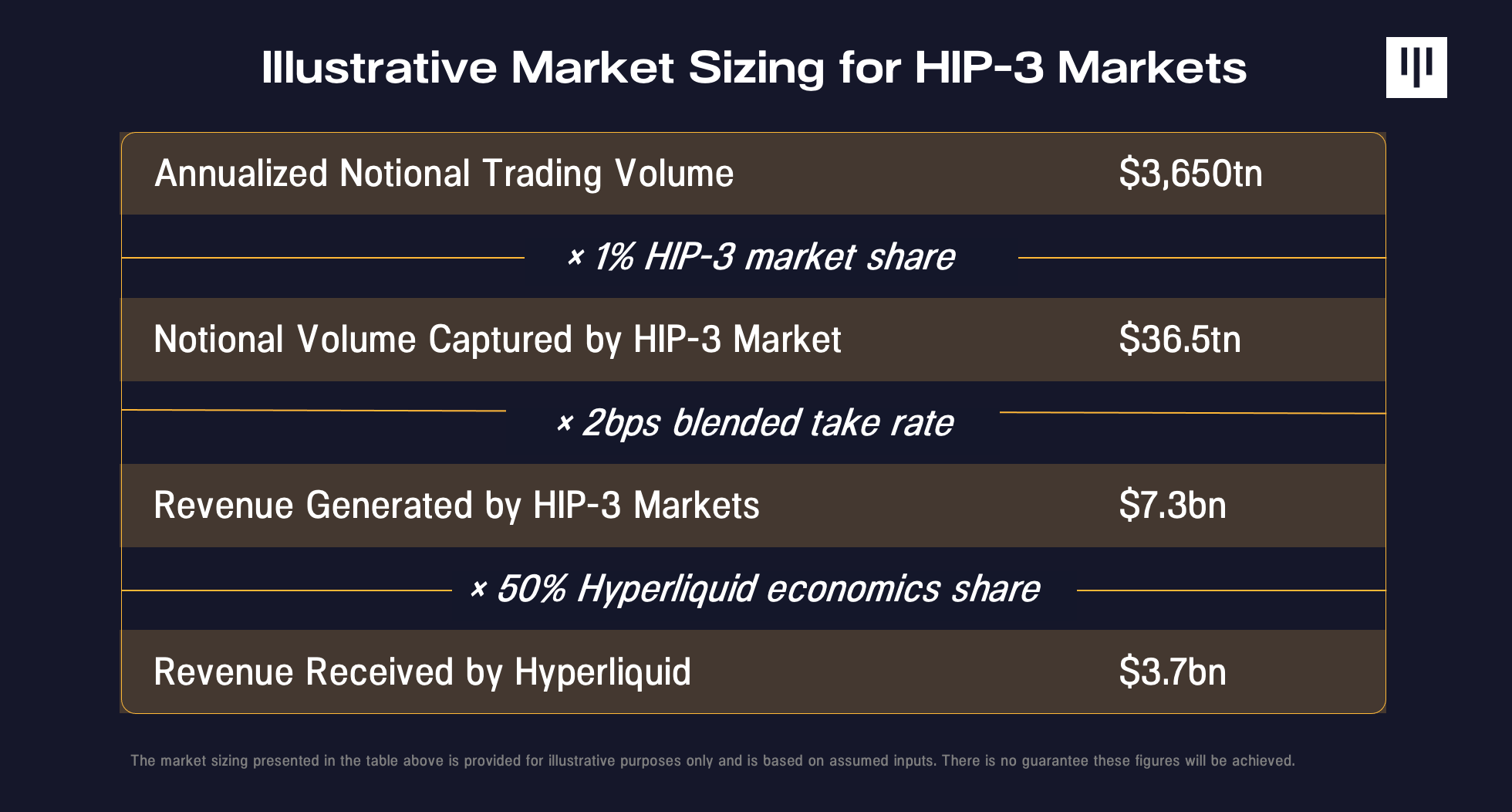

Hyperliquid has two properties native to blockchain that have helped it succeed in expanding its aperture to traditional assets typically traded on legacy exchanges. The first is that, as a decentralized exchange, Hyperliquid is open 24/7 by default, including on weekends and holidays. This compares to traditional exchanges like NYSE or CME which are only open five workdays a week. The second property is that Hyperliquid is permissionless, meaning any third-party can quickly list the assets people want to trade the most. Listed markets aren’t restricted to the imagination of the original Hyperliquid core team. Permissionless listings were unlocked by Hyperliquid Improvement Proposal 3 (HIP-3), which is a framework that allows any third party to permissionlessly list new perps markets and incentivize them with a share of transaction fees. An independent group operating under the trade.xyz brand has been the most prolific deployer.

As a result, the Hyperliquid platform has been able to adapt quickly to attract volume in whatever is the most topical asset at the time, including when traditional markets are closed, and the results have been striking. On-chain perps are becoming a parallel, always-on derivatives venue that is starting to meaningfully compete with traditional infrastructure. The clearest evidence is during moments of stress outside traditional trading hours. When gold and silver prices took off late 2025, Hyperliquid was the only venue on which it was tradeable on the weekends including that moment when China announced collateral requirement changes on silver trading. Silver briefly hit 2% of global derivatives volume at peak. When the Iran conflict started on a Saturday morning at the end of February, Hyperliquid was the only venue on which people could trade oil that weekend and daily crude volume surged to $3.7B. When oil futures opened Sunday night, they opened at the price oil perps were trading at already on Hyperliquid. Oil trading has reached 2% of global oil derivatives volume at peak. A month later, a fully licensed S&P 500 perp crossed $100M in volume on its first day. Traditional assets have at times reached as much as 40% of Hyperliquid’s volume, from essentially zero in late 2025.

Mainstream is Now Paying Attention

Hyperliquid’s traction has gained mainstream awareness this year. We are hearing more traditional asset hedge funds referencing Hyperliquid prices and even consider trading on the venue in order to be able to react to world events in a timelier manner.

Hyperliquid is becoming the exchange on which price discovery happens when all other markets are closed. Increasingly, this doesn’t just mean weekends, but also private companies prior to an IPO. On the day of Cerebras’ IPO (the largest IPO year-to-date), the banks underwriting the IPO were monitoring prices on Hyperliquid. A picture circulated showing Hyperliquid’s trading interface on a banker’s screen prior to the opening trade,

Wall Street exchange incumbents are paying attention as well. On May 27 at Bernstein’s Strategic Decisions Conference, Jeffrey Sprecher, founder and CEO of Intercontinental Exchange, called Hyperliquid “bigger than Nasdaq” and noted that ICE had met its founders several times. Just two weeks prior, it was reported that ICE and CME were pressing regulators to rein in Hyperliquid[7], a sign they view this as a real competitive threat. The significance is that one of the world’s major exchange operators is now openly acknowledging Hyperliquid as a serious competitive challenge rather than a fringe experiment.

Interest is showing up in public equities, too. Hyperliquid Strategies Inc. (NASDAQ: PURR), the digital-asset treasury (“DAT”) dedicated to Hyperliquid that Pantera was an anchor investor in, holds HYPE on its balance sheet and is chaired by Bob Diamond, former CEO of Barclays, with David Schamis as CEO. The two have taken the case for HYPE directly to mainstream U.S. financial media, including on CNBC’s Squawk Box[8] and Bloomberg[9], bringing a traditional-finance pedigree and credibility to a crypto-native asset to spread awareness. PURR has traded up over 200% year-to-date as of June 1, 2026 and is one of the few DATs sustainably trading at a premium to NAV, implying strong demand.

The next catalyst to watch is the SpaceX IPO, reportedly targeting later this month. There is a SpaceX perp on Hyperliquid, giving traders a way to express a view on where the company will price before it becomes available to public equity investors on NASDAQ. SpaceX is currently trading around $200 per share[10] as of June 1, 2026 on Hyperliquid, or above where bankers are rumored to want to price the stock. Every market participant is watching this IPO and it’s reasonable to expect that Elon Musk, SpaceX’s well-known terminally online and crypto-supporter CEO, may push both bankers and prospective investors to consider where SpaceX is trading on Hyperliquid, in turn driving a step function increase in awareness for the platform.

How Big Could This Get

Hyperliquid is an onchain protocol whose capital structure is token-based. HYPE is the native token through which Hyperliquid’s protocol economics accrue value, most visibly through the platform’s programmatic buyback mechanism using 99% of revenues – a capital allocation policy similar to many fundamentally valuable stocks. The investment case for Hyperliquid is premised on a few pillars:

- ■ Massive and Growing Target Market: Hyperliquid is a disruptive platform targeting an attractive, expanding end market. Perpetual contracts (perps) are an innovative product that serves large swaths of investors better than traditional derivatives, historically monetizing at highly attractive transaction fees. As Hyperliquid expands from crypto-native markets toward its goal of “Housing All of Finance,” its total addressable market multiplies.

- ■ Strong and Execution and Scale Flywheel: The protocol has captured significant market share by scaling faster and more successfully than prior iterations of decentralized perp exchanges. In this market, scale creates a flywheel advantage: higher volume drives order book liquidity, which continually improves the user experience and attracts more capital.

- ■ Superior Product Experience: Hyperliquid delivers premium user experience by operating on its own custom Layer 1 blockchain built specifically for derivatives trading. User feedback has consistently highlighted that the platform vastly outperforms other decentralized exchanges and directly rivals the speed and UX of major centralized exchanges.

- ■ Direct and Powerful Value Accrual to Tokenholders: Crucially, these strong fundamentals translate directly into protocol profitability and token value. Hyperliquid generates $800M in annualized revenue[11], nearly all of which is funneled into its programmatic token buyback mechanism. This creates an uncommonly tight alignment between protocol growth and tokenholder value.

Zooming out, Hyperliquid’s TAM is on the order of $10T of daily notional trading volume. There is roughly $200B per day of equities volume in 0DTE options and leveraged ETFs, the current tools investors use for simple high-leverage directional exposure. Commodities derivatives trade $2T in daily volume, and Hyperliquid has shown it can make inroads especially on holidays and weekends. FX derivatives which trade roughly $8T per day and are almost entirely untapped on-chain, making them a big greenfield opportunity. Capturing even a low single-digit percentage of that combined volume sustainably implies a revenue potential 5x that of today, and presumably a similar valuation expansion potential.

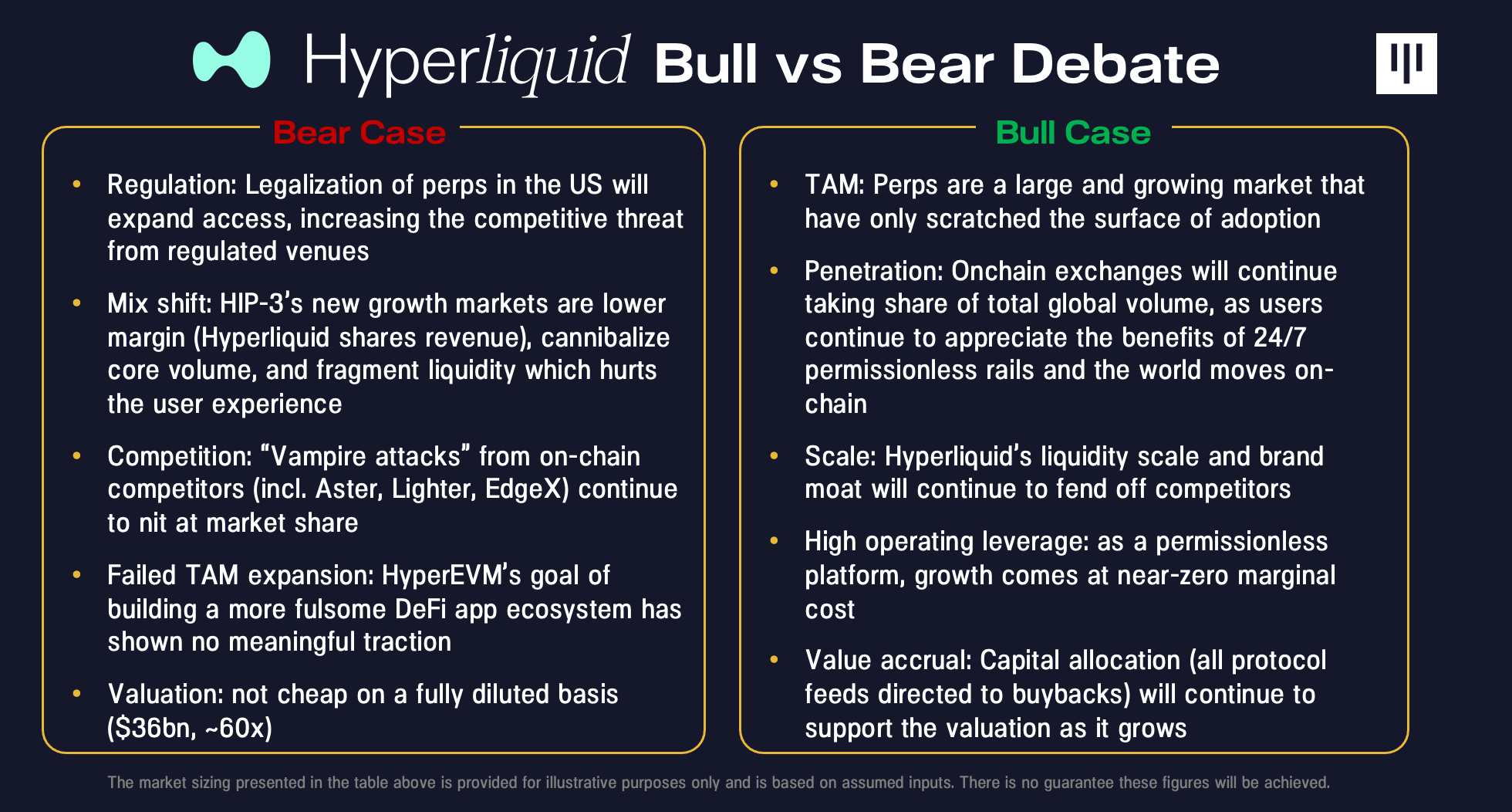

That said, there are real risks to Hyperliquid as well and it is important to acknowledge that. The biggest risk to Hyperliquid is regulation. Perps are not currently freely available in the US, although there has been a move toward legalizing and listing them. Hyperliquid is a decentralized exchange which means it does not have KYC requirements, and while it geofences against US users it is not impossible to think there are workarounds. If perps are legalized in the US, the competitive set gets more serious for Hyperliquid and it could possibly lose volume share from US users moving to a regulated venue. One mitigant is that it’s also possible Hyperliquid launches a US regulated instance of the exchange, as others have.

Regulatory Developments: The Door Opens

The single largest constraint on the growth of perps in the U.S. has been regulatory, and it is the same uncertainty that pushed Hyperliquid’s team offshore to Singapore. True perpetual futures have not been available to U.S. persons, and both centralized and decentralized venues geofence American users.

That began to change last week. The CFTC approved a bitcoin-referenced perpetual futures contract submitted by Kalshi’s US registered exchange, and its staff separately cleared the way for Coinbase to offer certain crypto perpetuals through a foreign affiliate, treating them as foreign futures. The throughline is that the CFTC has opened a path for regulated crypto perps under existing futures frameworks, rather than demanding entirely new rulemaking. Some policy advocates believe that the historical absence of perps in the U.S. was less a deliberate regulatory choice than a commercial accident of which products incumbents chose to list, and that there was never a fundamental reason the CFTC could not permit them. The CFTC would just have to move now to make that clear if and when exchanges apply for more perps listings.

The harder question is what it takes to bring decentralized perps to U.S. users, and here the path is less clear. A centralized actor can register as a U.S. exchange today, and we have seen that others like Coinbase and Kalshi want to list real perps. For a permissionless onchain protocol, the Commission would need to extend exemptions, both from the requirement that derivatives trade on a registered exchange and from the rules on who may access certain contracts. The SEC and CFTC both have a pro-innovation stance and have previously made statements that support the idea that nothing in an onchain protocol’s core stack inherently requires registration. However, preserving permissionlessness and the absence of KYC while satisfying legitimate concerns around sanctions and market integrity will take some work to figure out.

Perps began at crypto’s edge because that was where market structure could evolve fastest. Perps are now moving toward the center of global finance. The recent CFTC actions do not resolve every regulatory question, especially for permissionless onchain venues, but they do mark an important shift. The U.S. is beginning to accommodate the product rather than dismiss it. Hyperliquid sits at the center of that transition. It has paired the best attributes of DeFi, which are open access, 24/7 markets, transparent settlement, and unusually strong stakeholder alignment, with a product that increasingly looks better suited to modern trading than the instruments it competes with. The question is no longer whether perps can matter outside crypto; the market is already answering that. The question is whether the infrastructure that the blockchain industry built first can become the place where the rest of finance increasingly prices risk, trades, and discovers.

[1] CryptoQuant, “FY 2025 Review of Crypto Exchange Activity”

[2] Coinglass, “2025 Annual Report”

[3] Artemis, TheBlock, Pantera analysis

[4] Blockworks Research, “Perp DEXs Analytics”

[5] Colossus, “Beyond the Sky: Jeffrey Yan & Hyperliquid” (April 2026)

[7] Bloomberg, “CME, ICE Push US to Curb Crypto’s Oil Trading Upstart”

[8] CNBC, “Sonnet-Hyperliquid Deal Approved, Merger Creates $1 Billion Crypto Treasury”

[9] Bloomberg, “More Real World Assets Are Coming On-Chain: Diamond”

[10] Hyperliquid, “SPCX Trading”

[11] Blockworks, Hyperliquid Annualized Revenue

This letter is an informational document that primarily provides educational content and general market commentary. No statements included herein relate specifically to investment advisory services provided by Pantera Capital Partners LP or its affiliates (“Pantera”), nor does any content herein reflect or contain any offer of new or additional investment advisory services. Nothing contained herein constitutes an investment recommendation, investment advice, an offer to sell, or a solicitation to purchase, any securities in Funds managed by Pantera (the “Funds”) or any entity organized, controlled, or managed by Pantera and therefore may not be relied upon in connection with any offer or sale of securities. Any offer or solicitation may only be made pursuant to a confidential private offering memorandum (or similar document) which will only be provided to qualified offerees and should be carefully reviewed by any such offerees prior to investing. Past performance is not indicative of future results. Investing in digital assets involves significant risk, including the potential loss of principal.

This letter is not intended to provide, and should not be relied on for accounting, legal, or tax advice, or investment recommendations. Pantera and its principals have made investments in some of the instruments discussed in this communication and may in the future make additional investments in connection with such instruments without further notice.

Certain information contained in this letter constitutes “forward-looking statements” (including predictions), which can be identified by the use of forward-looking terminology such as “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue”, “believe”, or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking statements, and no undue reliance should be placed on these forward-looking statements. There is no guarantee that investments in any instrument or type of instrument described herein will be profitable – all investments carry the inherent risk of total loss.