Investing in Four Pillars

June 1, 2026 | Jonathan Gieg

![]()

The Bridge to Korea

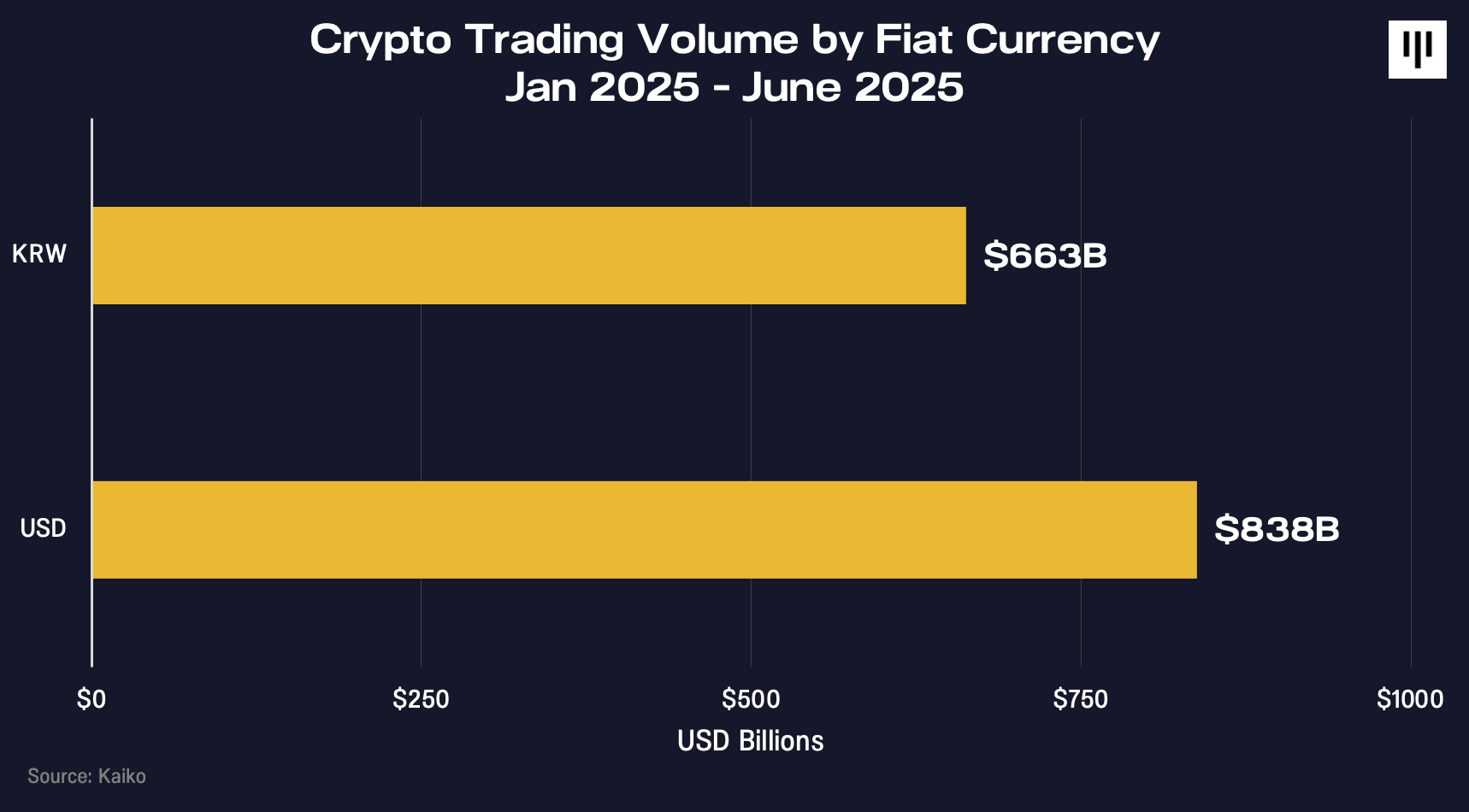

In the first half of 2025, Korean won–denominated crypto trading volume reached $663 billion, behind only the US dollar at $832 billion (Kaiko, June 2025). That means a single national currency, used by a population of roughly 52 million, is the second-largest fiat denomination in global crypto markets.

By late 2025, industry data counted 11.13 million active Korean crypto investors (Korea Financial Intelligence Unit (KoFIU) and Financial Supervisory Service (FSS), Survey on Virtual Asset Service Providers, Second Half of 2025) — more than 1 in 5 of the entire population — generating daily average trading volumes of approximately $4 billion, even after a 15% half-over-half cooling. Korea is also one of the highest-adoption markets globally for new technology more broadly: OpenAI identified Korea as the largest ChatGPT market in Asia-Pacific in September 2025, and Anthropic’s Economic Index ranked Korea among the top countries globally for Claude usage per capita in January 2026. The pattern that now defines AI adoption in Korea showed up in crypto first.

This is not a niche market, but it operates on a fundamentally different set of rails than the West.

A Market Built Differently

Korea’s distance from Western crypto isn’t really about isolation. It’s about a market that has developed on its own terms, with its own cultural and structural model that rewards genuine engagement and punishes shortcuts.

What stands out most is not just trading activity, but a cultural willingness to pay for innovation. Across every new technology cycle — from broadband to mobile to crypto to AI — Korean consumers and institutions adopt early, adopt deeply, and pay for quality. That cultural posture is a structural advantage that compounds over time.

But despite this dynamism, a meaningful gap remains between Korean talent and the global networks that shape crypto’s largest capital flows and product surfaces. Language is part of it. Physical distance is part of it. So is the simple reality that most Korean investment theses are written and circulated in Korean first, translated days or weeks later, if at all. Western funds reading English-language coverage are systematically late to the most important market structure shifts in Asia, and Korean teams building world-class infrastructure often struggle to be heard outside their home market.

We believe this is a coordination problem, not a permanent feature. Someone needed to take the initiative to bridge Korean retail and institutional participants with the global crypto economy. We believe Four Pillars is uniquely positioned to play that role.

Why Four Pillars

We believe Four Pillars is the most important independent crypto research firm in Korea. Founded in 2023 and based in Seoul, the team has built one of the rare research operations that meaningfully bridges the institutional and retail layers of the Asian market. Their researchers, including Steve Kim, Jay Jeong, Jinsol Bok (“100y”), Heechang Kang, and the rest of the analyst team, are regularly cited by Bloomberg, The Korea Times, AMBCrypto, and the leading Asian financial press. They also co-founded the Asia Stablecoin Alliance with the Head of APAC at LayerZero to coordinate cross-border stablecoin infrastructure across the region as well as the Hyperliquid Research Collective with GLC Research, one of the most well-known research institutions in the Hyperliquid ecosystem.

Four Pillars is selective by design and has dedicated partners that include Sui, LayerZero, Monad, Arch, Stable, Walrus, and Rialo. Long-term partners include Securitize, Pudgy Penguins, Ondo Finance, Ethena, EigenCloud, Cap, DoubleZero, Spark, and more.

What sets Four Pillars apart from typical research-for-hire shops is the operating model. They are conviction-driven rather than pay-for-play. They have earned the trust of Korean government officials, financial institutions, top-tier KOLs, and both Web3-native and mainstream Korean media. This is a combination of access points that is exceptionally difficult to assemble. In our conversations with their existing customers, the consistent pattern was the same: high integrity, strong execution, and a unique ability to operate credibly across institutional, retail, and policy audiences in Korea.

The firm is now expanding beyond research into validator infrastructure on PoS networks, as well as advisory networks and seminars tailored for institutions. This represents a natural extension of its research-driven foundation. Four Pillars’ deep protocol-level expertise, combined with the strong relationships it has organically built with global leaders, creates a sustainable flywheel for a wide range of industry participants to grow alongside global trends, generate synergies, and compound together over time.

What This Partnership Unlocks

Four Pillars is the connective tissue we have been looking for between Pantera’s portfolio and the Asian market.

For both sides, this is a research and intelligence partnership. Four Pillars’ on-the-ground perspective on Asian regulatory developments, conglomerate strategy, and capital flows will inform Pantera’s investment process across stablecoins, tokenization, and Asian market structure. Pantera’s global vantage point and portfolio depth will inform Four Pillars’ research agenda. Together, we are positioned to co-develop theses on the questions that matter most for Asian crypto over the next several years: which KRW stablecoin model wins; how tokenized securities in Korea integrate with global on-chain credit markets; how Asian conglomerates’ platform-and-payments approach to crypto compares with the treasury-strategy model dominant in the United States, and more.

Our first piece of collaborative research was a 155-page Blockchain Guide for Korean Institutions, written to help them prepare for the onchain era.

Why Now: Korea Is at a Regulatory and Institutional Inflection Point

The last 18 months have produced more concrete change in Korean crypto policy than the prior eight years combined.

Security token offerings (STO) are no longer a regulatory gray zone.

On January 15, 2026, the National Assembly passed amendments to the Capital Markets Act and the Electronic Securities Act, formally legalizing the issuance and trading of tokenized securities on distributed ledgers across debt, and investment contract products that took more than three years of groundwork after the FSC first issued STO guidelines in 2023. The law is expected to take effect in January 2027 following a one-year preparation period, and would open a regulated pathway for tokenized real estate, bonds, fund structures, music copyrights, and shares of unlisted companies.

The Digital Asset Basic Act

Expected to pass in late 2026, with timing likely shaped by the June presidential election, this legislation will replace the term “virtual assets” with “digital assets” and reauthorize domestic ICOs for the first time since the 2017 ban. It will require all stablecoin issuers to maintain 100% reserves in bank deposits or government securities, and it will provide the first unified rulebook for issuance, trading, and consumer protection.

KRW stablecoins are the central battleground

Eight major commercial banks — including KB Kookmin, Shinhan, Hana, Woori, NongHyup, IBK, Suhyup, and SC First Bank — are developing a shared won-pegged stablecoin under unified infrastructure. KB Kookmin alone has filed more than a dozen trademarks tied to a “KB KRW” stablecoin. An early publicly disclosed pilot, KRW1, launched on Avalanche in September 2025 through a partnership between digital asset custodian BDACS and Woori Bank, with each token fully collateralized by Korean won held in escrow.

The conglomerate layer is moving in parallel. Upbit’s pending $10.3 billion acquisition of Dunamu, the operator of Upbit, faces a shareholder vote in May 2026; if approved, it would create the only entity globally with exchange, payments, search, and AI infrastructure in a single stack with Upbit’s Q1–Q2 announced Layer 2, Giwa, for stablecoins and payments. Kakao, with 49 million monthly active users on KakaoTalk, is building stablecoin infrastructure through KakaoBank. Separately, the Kaia chain (the merged Klaytn × LINE blockchain) has filed trademarks for KRWKaia and KaKRW. Samsung Wallet is in active discussions with Shinhan and Hana to provide the offline distribution layer for whichever stablecoin wins.

Tokenization is the second-order opportunity

Boston Consulting Group estimates that Korea’s fractional investment and security token offering market could reach ₩367 trillion ($250 billion) by 2030. The Financial Services Commission is set to approve an over-the-counter market for tokenized securities in early 2026. Korean Treasury Bonds (KTBs), already core High-Quality Liquid Assets in the domestic financial system under Basel III, are a natural collateral base for the kind of on-chain structured products that have already proven product-market fit globally through BlackRock’s BUIDL and Franklin Templeton’s BENJI.

It seems as though every meaningful actor in Korean finance is in motion at the same time.

Korea’s distinctive RWA collateral base

One of the sharpest insights from our joint work is how unusual Korea’s position in real-world asset tokenization actually is. Global exotic RWA experiments to date have been upstream and commodity-driven such as tokenized uranium, GPU compute, mineral royalties, and oil and gas. Korea sits at a different point in the value chain entirely. The country doesn’t mine uranium, but Korean firms hold an $18.6 billion EPC backlog for nuclear plants like Dukovany. Korea doesn’t design GPUs, but SK hynix and Samsung together control roughly 80% of the global HBM market that powers them. Korean shipbuilders carry more than 70% of global orders and dominate the LNG carrier segment. These are contract-driven cash flows — long-tenor, counterparty-credit-anchored, frequently denominated in dollars — that fit Korea’s STO framework cleanly and would be hard to replicate from any other national base. As the legal infrastructure activates in 2027, the natural collateral pool emerging here looks structurally different from anything being built on-chain elsewhere.

Agentic commerce as the KRW stablecoin’s natural use case

A second thesis we’ve been developing together concerns where KRW stablecoins actually win. Korea’s payment infrastructure is already world-class. Cash usage fell to 15.9% in 2024, simple-payment volume runs over a trillion won daily, and the existing rails leave little room for a domestic stablecoin to win on speed or cost alone.

The interesting opening is somewhere else: agentic commerce. Machine-to-machine payments, sub-cent API calls, and headless merchant endpoints sit outside the economics of card networks. The x402 protocol alone has processed roughly 109 million transactions since launch, settling at fees below $0.001 each. This is the surface area where a KRW stablecoin has structural advantages that traditional rails cannot match, and it’s why KakaoPay’s recent decision to join the x402 Foundation is more meaningful than it might look. The KRW stablecoin race in Korea has been framed as a question of which consortium issues first. The more interesting question, and the one our work together is increasingly focused on, is which actor builds the agentic commerce stack that gives the stablecoin a reason to exist.

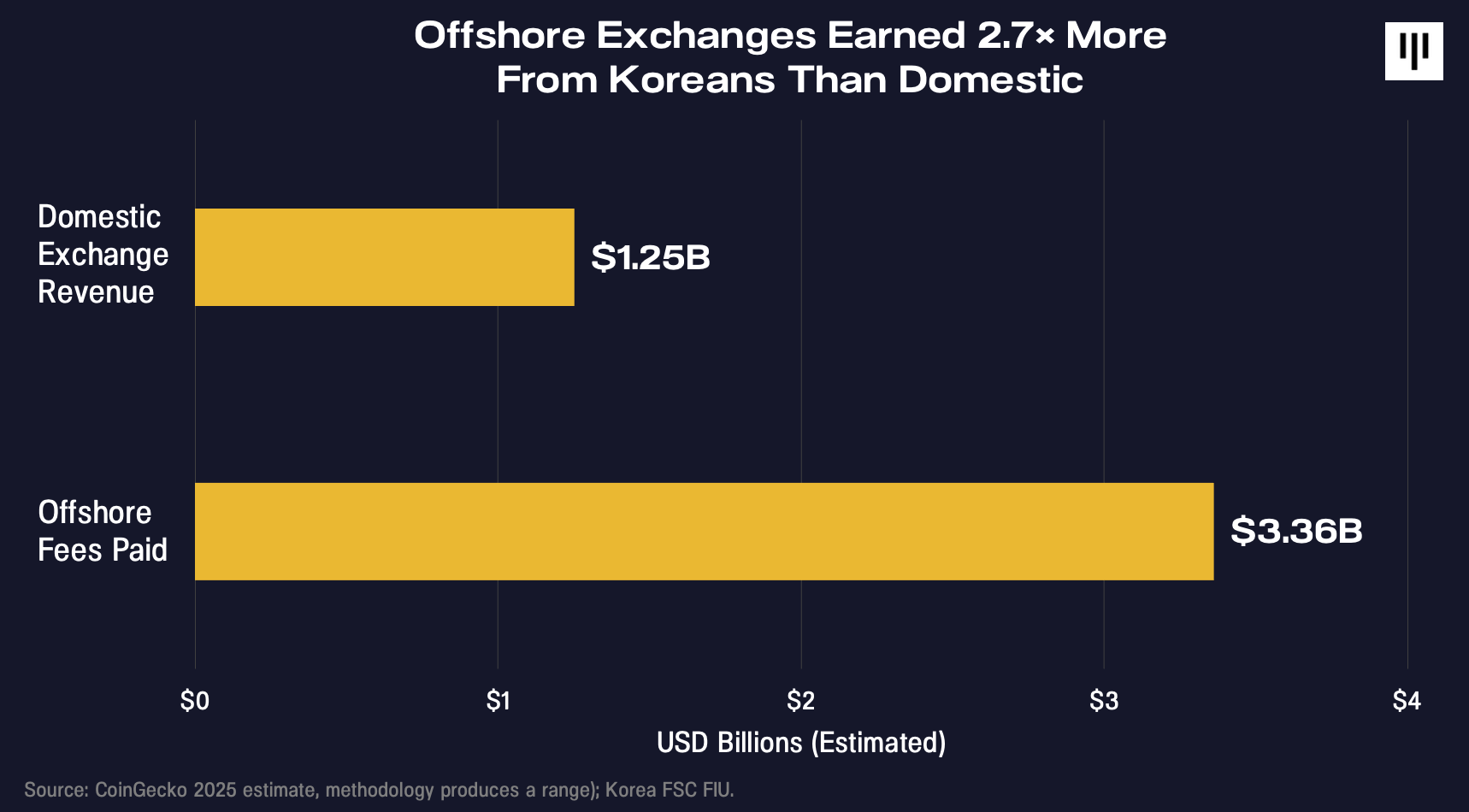

The $110 Billion Demand Signal

There is a second statistic from 2025 that should reframe how Western investors think about Korea. According to a joint report from CoinGecko and industry data, an estimated ₩160 trillion (~$110 billion) flowed from Korean exchanges to overseas platforms during 2025, primarily Binance, Bybit, OKX, Bitget, and Huobi. The same report estimates fee income from Korean users on those five offshore exchanges reached approximately $3.36 billion for the year. (Both figures are estimates derived from on-chain flow tracing and benchmark assumptions; the underlying methodology produces a range, not a precise number.)

This is not a sign of weakness in Korean demand. It is a sign of the opposite: Korean retail and emerging institutional capital is sophisticated, mobile, and actively seeking products and venues that the constrained domestic market cannot offer. They want access to things like perpetual DEXs, structured products, advanced derivatives, and global altcoin exposure. Whoever bridges the gap between Korean capital and global crypto product surface area will capture an enormous, durable opportunity.

The Future of Crypto in Asia Runs Through Korea

The global conversation about crypto remains disproportionately focused on the United States. That focus is increasingly out of step with where actual on-chain activity is happening. Asia is the largest geographic source of stablecoin transaction volume globally and a part of the world Pantera has invested in for years. Singapore is our second-largest home for portfolio company founders outside the United States, and roughly 40% of our capital has been deployed into companies headquartered abroad. Now we believe Korea is the second-largest national crypto market in the world. The infrastructure being built in Seoul like bank-led but tech-distributed stablecoins, vertically integrated super-app crypto stacks, and sovereign-grade collateral on-chain has no direct analog in any Western market.

And not only Korea is taking actions. Japan licensed JPYC as its first regulated yen stablecoin in 2025, while MUFG, SMBC, and Mizuho jointly build a megabank-issued stablecoin through Project Pax. Hong Kong passed its Stablecoins Ordinance and granted the first two issuer licenses, to HSBC and a Standard Chartered–led JV.

Four Pillars sits at the center of this transition: trusted by government officials, financial institutions, exchanges, covered in Bloomberg and The Korea Times, and embedded in the strategy conversations at every major Korean conglomerate moving into digital assets. They are the firm we trust to enable Asian builders and companies to connect with Pantera’s global portfolio, and the firm we trust to help us understand what is happening in Asia before it shows up in English.

We are proud to lead their Series A round.

If you are a founder building in crypto and serious about reaching the Asian market, or an Asian team building toward global liquidity, connect with the Four Pillars team at support@4pillars.io or reach out to Pantera directly.

Disclaimer:

This document is made available by Pantera Capital Partners LP (“Pantera”) for informational and educational purposes only. It does not contain all information pertinent to an investment decision. Nothing in this document constitutes an investment recommendation or an offer of investment advisory services. This document cannot be relied upon in making an investment decision. Nothing contained herein constitutes an offer to sell, or a solicitation to buy, any securities. This document contains information believed to be reliable, and has been obtained from sources believed to be reliable, but no representation or warranty is made (express or implied) of any nature, nor is any responsibility or liability of any kind accepted, with respect to the fairness, accuracy, completeness, or reasonableness of the information or opinions contained herein. Forward-looking statements should not be relied upon. There is no guarantee that investments in any instrument described herein will be profitable – all investments carry the inherent risk of total loss. Analyses and opinions contained herein (including market commentary, statements or forecasts) reflect the judgment of the author as of the date this document was published, and may contain elements of subjectivity (including certain assumptions) or be based on incomplete information. There is no duty or obligation to update the contents of this document. This document is not intended to provide, and should not be relied on for accounting, legal, or tax advice, or investment recommendations. Pantera and its principals have